Real estate world in flux.

Real Estate. The demands on players in the real estate industry are changing rapidly. "More than ever before, investors have to view each property as an independent corporate commitment and, above all, keep an eye on ESG aspects," analyse Thomas Wiegelmann, Managing Director at Schroder Real Estate, and Jan Linsin, Head of Research at CBRE in Germany.

Like all areas of our lives, the real estate industry is currently undergoing rapid change. The interruption of many business operations and the partial suspension of rent payments during the pandemic have shattered the myth that landlords are disconnected from the business success of their tenants. Environmental awareness and responsibility are adding to the demands.

"More than ever, the need for functioning operational partnerships between owners and tenants is accentuated," makes Thomas Wiegelmann, managing director at Schroder Real Estate, clear. His opinion carries weight. After all, Schroder manages 4.86 billion euros in the real estate sector in Germany, Austria and Switzerland. In the past months of the Corona pandemic, the investment manager explains, it has been made crystal clear to investors that this type of capital investment always means "co-ownership" of the operating risk of the companies of their tenant clients that use the building.

As a consequence, analyses Jan Linsin, Head of Research at CBRE in Germany, owners and investors should now rethink their real estate exposure altogether: "More than ever, each property needs to be managed as a standalone business to ensure longer-term revenue and value creation, limit carbon emissions and waste, and prevent obsolescence." This, she said, requires much more specialized real estate expertise on the part of the investor.

Real estate management of the future, the experts say, will be characterized by flexibility, innovation and cooperation. And is geared much more clearly than before to the tenants' business models. "Only in this way can investors anticipate the rapid changes in the real estate market at an early stage," Wiegelmann is convinced.

Examples illustrate how dramatically the market has changed. In the last five years, the average vacancy rate in Europe's shopping centres has doubled, and between 2015 and 2020, the number of serviced office and co-working spaces quintupled, according to CBRE. E-commerce is depressing demand in retail real estate - with the explicit exception of grocery stores and local suppliers - and causing it to explode in logistics. Changing work habits require flexible, hybrid work concepts and are making some office space redundant. New healthcare considerations are changing the density of users in offices and increasing the need for additional space. "Real estate investors who work in partnership with their tenants will be able to successfully anticipate emerging trends and reflect them in their real estate strategy to create value," says Wiegelmann.

First and foremost, Jan Linsin cites the sharing of business-critical information. "If the real estate owner better understands the critical factors for the tenant's business success and receives timely information, he can adjust space offers, services and contractual terms throughout the duration of the business relationship. This not only improves the tenant's business prospects, but also benefits the landlord in the long run." "The parties involved in any negotiation should not strive for their own optimal outcome, which can only be achieved to the detriment of the other party. Instead, the aim is to create win-win situations," adds Thomas Wiegelmann.

Specifically, the experts expect that tenants in many areas will tend to seek shorter lease terms and a higher degree of flexibility in the future. For their part, landlords could offer turnover rent components with lower fixed rents.

Sustainability will also be a clear priority in the real estate industry in the future. According to the Global Alliance for Buildings and Construction, the built environment is responsible for around 40 percent of global CO2 emissions. "The real estate industry is therefore seen as key to achieving the European Union's zero emissions target by 2050," explains Linsin. Sustainable buildings consume few resources and have a lower impact on the environment.They thus optimised the long-term value for their owners and users. "Quantifiable sustainability of real estate will become an indispensable quality feature that encompasses the life cycle and the entire value chain," Wiegelmann explains, "in this context, sustainable refurbishment in existing buildings will be a key challenge."

Here, too, it is important for landlords and tenants to work together more intensively, he adds. "One example is the joint analysis of operating data and costs," suggests Linsin. If data on the actual use of the building is exchanged in detail, massive improvements can be achieved. "Room design can be optimised, electricity and water consumption minimised, waste reduced and CO2 emissions massively reduced."

The biggest difficulty, he says, is finding ways to accurately measure resource use in multi-tenant facilities without violating their privacy. "The conditions are there," Linsin makes clear, "a number of technology solutions and mobile apps have already been developed that control access to buildings, provide directions to desks and meeting rooms, and allow employees to control temperature and lighting. We just need to convince everyone concerned to use them."

Specifically, these apps work in combination with sensors and controls built into locking systems, heating and ventilation systems, and lighting - a real-world example of the Internet of Things.

"This can also result in a win-win situation," explains Thomas Wiegelmann. "Research shows that employees who can control their own heating and ventilation are happier and more productive. Detailed data on energy consumption can also help building managers optimize heating and cooling and avoid waste, focus cleaning staff on hotspots, and identify faults in equipment before they become serious. This leads to lower utility and service charges and ultimately prevents premature aging."

Because investors are increasingly considering ESG criteria in their investment decisions, he said it is imperative for investment managers to also anticipate and incorporate them into their investment decisions. "In the future, investors and tenants alike will divest themselves of properties that pose a significant sustainability risk - this then implies a risk of price discounts for corresponding assets," Wiegelmann makes clear. At present, ecological aspects are still at the forefront. "However, social goals and a fairer economy will also become increasingly relevant for the performance of individual properties in the future," says Linsin.

"As a result of the market upheavals caused by Covid-19, there are great opportunities for investors," concludes Thomas Wiegelmann, "in order to take advantage of these, specialised know-how in real estate investment and asset management is needed more than ever. Owners who fail to recognise this will lose ground to flexible owners - and ultimately the chance to meet or improve their performance targets."®

–––––––––––––––––––––

// Global Real Estate Market - Back to Old Strength in 2021.

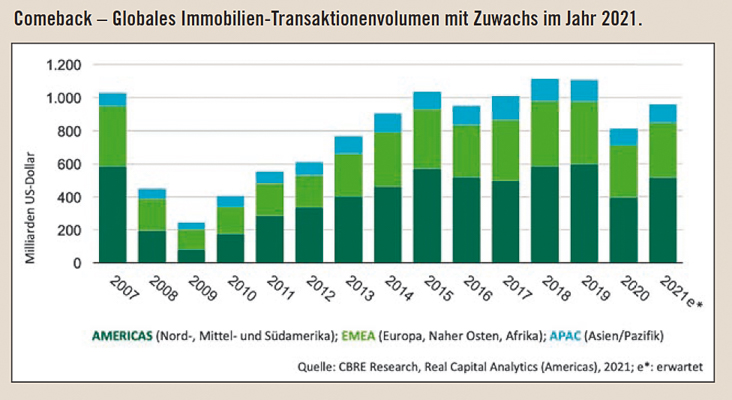

In global commercial real estate, the Corona crisis is all but over. CBRE, the world's largest commercial real estate services company, expects global investment volumes to grow by 15 to 20 percent year-on-year in 2021. This should then almost return to the level of 2019 (chart below).

"This will be driven primarily by a strong upturn in North America, where, according to our recent investor survey, 70 percent of investors plan to invest 20 percent more in 2021," informs Jan Linsin. Buoyed by the $1.9 trillion stimulus package, US investor confidence is already particularly robust, he adds. "And the second half of 2021 is then expected to see a further, significant increase in transaction volumes as the US and UK could achieve herd immunity."

The German real estate market also continues to gain in importance internationally. "It is considered a comparatively safe haven for real estate investments. According to our survey, both national and international investors rate the prospects for a rapid recovery of the real estate investment market after the pandemic in Germany as the best within Europe. With Berlin, Frankfurt, Hamburg and Munich, four German metropolises are also among the top ten most attractive European cities for real estate investments," explains Jan Linsin.

In fact, the transaction volume on the German real estate market in the crisis year 2020 still amounted to more than 90 billion dollars. "That was only five percent less than in the previous year. In 2021, thanks to stable domestic demand plus international interest, investment momentum should remain very high. Only the supply situation of low-risk core and core-plus properties is currently a limiting factor," says Thomas Wiegelmann. "The decisive factor here is the expectation of many investors that the comparatively solid state finances in this country will allow them to continue to offer generous financial aid and thus prevent a rapid rise in unemployment or insolvencies even after the emergency measures have been discontinued," clarifies Jan Linsin.

The current and future German government would be well advised to keep the country attractive as a business and investment location for international companies and investors. In this context, less market intervention and market regulation would be appropriate. In many areas, the public sector simply does not provide the urgently needed real estate and infrastructure. "Private capital must therefore play the decisive role so that, for example, (affordable) housing for young and old or social and educational facilities can be built in liveable and ecologically sustainable cities," the real estate professionals make clear.

–––––––––––––––––––––

// Portfolio strategies according to Corona - real estate investments under the microscope.

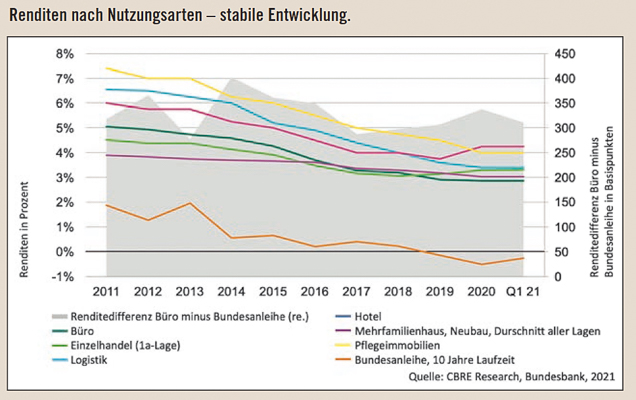

"The German real estate industry has come through the Corona crisis comparatively well," Jan Linsin states, "in general, no Corona-related price reductions could be proven in 2020 for core properties that are in high demand. Prime yields remained stable there. Only non-food retail and hotel properties saw yield reductions over the course of last year." Linsin also expects the solid development to continue, especially because the very expansive monetary policy of the European Central Bank (ECB) should continue for some time.

In general, the experts at CBRE and Schroder Real Estate believe that the Corona pandemic will not stop the trend of further urbanization. Cities with diversified economic structures, growth industries, good educational institutions and high quality of life will continue to grow, generating demand for space. "We see a clear trend that locations with a high quality of stay and clearly mixed use in particular will be among the winners," explains Thomas Wiegelmann: "Here, living and working are combined with shopping, gastronomy, leisure use, entertainment, health infrastructure and administration. Properties in increasingly monostructural locations will come under pressure."

The professionals took a closer look at the individual types of use:

// 01. Multifamily

Due to the atomized tenant structure and high granularity of rental payments, this asset class is very defensive and stable. There continues to be a shortage of supply in metropolitan areas of growth regions. The trend towards rising rents and purchase prices is therefore likely to continue in these regions in the medium term. Investor interest is also increasing in properties on the outskirts of metropolitan areas and in attractive B and C cities.

02. office properties

Modern, high-quality office properties continue to be in favour with investors and users, while lower-quality office properties are coming under increasing pressure. Changing working habits call for flexible workplace concepts. Many companies have switched to home offices, and it can be assumed that spatially flexible, hybrid work will permanently gain in attractiveness and acceptance. Instead of the "standard office floor plan", there will be different floor plans for different categories of users in the future. For example, new office spaces could take on the role of centrally located headquarters for "clients and brands", acting as fully equipped and flexible "community culture centres".

03. retail

This segment shows a wide spread between the different formats. Modern grocery closeout to meet daily needs continues to be a very attractive asset class that has proven resilient, particularly in the Corona pandemic. The losers, on the other hand, include shopping centres without a clear unique selling proposition, which also do not invite people to stay longer.

This trend, already apparent before the pandemic, is now accelerating and will lead to further closures.

Unless they are actively and innovatively managed, retail properties in B locations or "secondary" shopping streets without a convincing quality of stay are also likely to become irrelevant in the future.

04. special properties

The steady rise in online trade and increasing demand from the recovering industrial sector continue to ensure high momentum in the logistics market.

Healthcare and social real estate are also experiencing increasing investor interest.

And last but not least, the rapidly advancing digitalisation, but also the integration of home offices in the Corona pandemic, are increasing the demand for computing power.This is now bringing data centres increasingly into focus as an alternative asset class.

–––––––––––––––––––––

Special Publication:

Dr Thomas Wiegelmann,

Managing Director of Schroder Real Estate

Asset Management GmbH,

and Dr. Jan Linsin, Head of Research at CBRE GmbH in Germany.