Industry in distress.

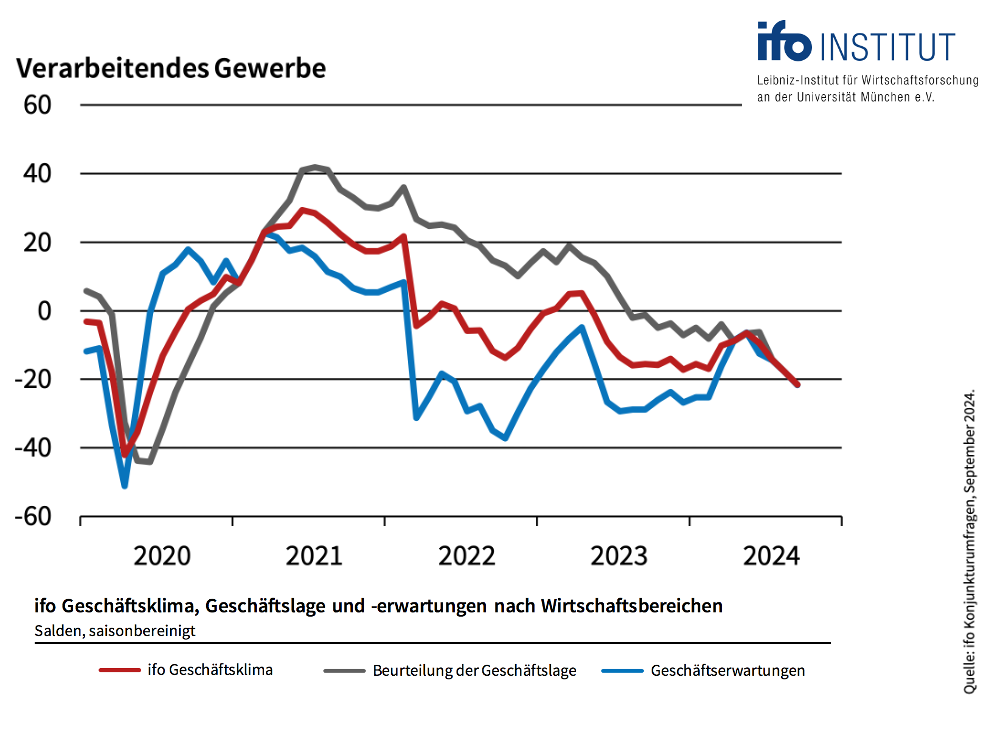

The core sectors of German industry are in trouble, according to the ifo Institute's latest business climate index for September. In fact, the business climate has been trending downwards since mid-2021 and has now reached its lowest level since the deep recession of 2008/2009 - at least if the three extreme coronavirus shock months in spring 2020 are excluded. The situation is bad, the lack of orders has worsened and expectations in the boardrooms are becoming increasingly pessimistic.

A month ago, the private wealth stock market indicator had already interpreted the dramatic deterioration in business expectations in industry as a downward economic trend reversal and reduced the equity allocation accordingly. Unfortunately, this negative assessment has now been confirmed. Companies are struggling with high costs and weak sales - an environment in which profit margins are likely to come under further pressure. A deterioration in the earnings situation of manufacturing companies is therefore to be expected in the coming quarters.

This is not a good environment for equity investors. The key question is therefore: How can it be that the DAX is trading at a high in this difficult fundamental situation?

First of all, the DAX reflects not only the German economy, but above all the international economy. And this is still on a moderate growth path. Furthermore, all-time highs on the stock markets are the rule, not the exception. Real growth and price increases mean that turnover and profits in the corporate sector increase continuously over time. This is why the prices of a broad index must also rise in the long term.

However, the emphasis here is on the long term. In the short term, there are always deviations from the trend. In times of euphoria, share prices often rise too quickly. If pessimism prevails, they fall below a reasonable level.

The private-wealth stock market indicator takes advantage of this by comparing the ‘fair value’ of the German stock market, determined by the editorial team on the basis of long-term economic components, with the current stock market levels and drawing appropriate conclusions.

From this perspective, the current constellation is indeed unusual. Despite the poor sentiment among companies, the German stock market is still trading slightly above its fair value. In similarly poor economic phases in the past, however, it usually fell to a level of between 75 and 90 per cent of its fair value. This shows how great the potential for correction could be if there are no signs of an economic turnaround soon.

The conclusion for investors:

The economy, specifically the business expectations of German industry, and the market valuation of the DAX define the strategic corridor for the equity allocation of the private wealth stock market indicator.

As the economic component is set to ‘red’ and the German stock market is trading at around the level of its ‘fair value’, this range lies between 45 and 75 per cent of the individually planned equity allocation. Should the DAX climb towards 20,000 points in the coming weeks, the analysis of the fair value would suggest a further reduction in the strategic range.

Within this corridor, the capital market seismograph - the third component in the private wealth stock market indicator alongside the economy and valuation - defines the exact positioning. The probability landscape of the seismograph has been very positive for a long time. This has not changed recently. On the contrary: the interest rate cut by the US Federal Reserve has further strengthened the positive probability picture. This is why the equity allocation in the private wealth stock market indicator remains at the upper end of the strategic corridor at 75 per cent.

An example: For investors who consider an equity allocation of 50 per cent to be optimal in the strategic allocation of their assets, the model would suggest investing only 37.5 per cent in equities (75 per cent of 50 per cent results in an equity allocation of 37.5 per cent). The proportion of cash in the portfolio would be increased accordingly in order to be able to buy in the event of any setbacks.

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided on the private-wealth stock market indicator is for information purposes only and does not constitute an invitation to buy or sell securities.