Cold shower for German industry.

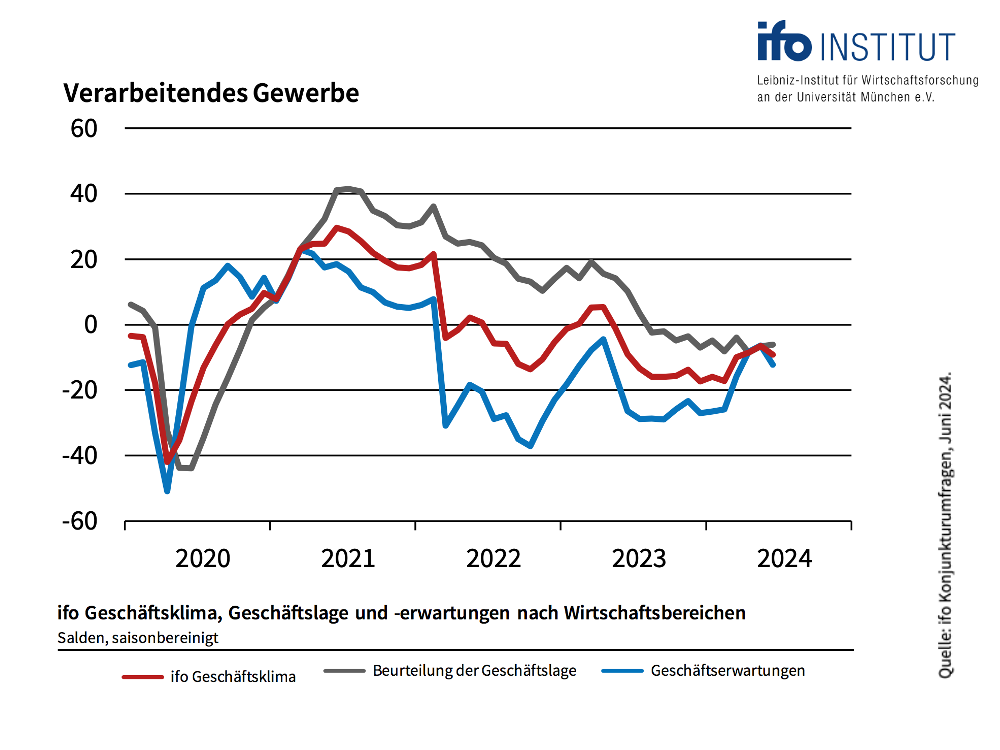

The ifo Business Climate Index for June shows a surprisingly significant decline in industry, which is so important for the private wealth stock market indicator. The index for business expectations in the manufacturing sector fell from minus 6.4 points to minus 12.3 points. This is the first decline since December 2023 and a clear damper on hopes for positive economic development in the second half of the year.

Why have company bosses suddenly become more pessimistic when the ifo Institute itself has just raised its economic forecast slightly and is now saying that the German economy is on course for recovery?

We suspect that two political developments have contributed significantly to this. One is the threat of tariffs on e-cars from China. If this were to trigger retaliatory measures, it could cause considerable economic damage for German companies that generate a large proportion of their revenue in the Far East. However, there is still hope that the trade dispute between Europe and China can be resolved amicably. After all, neither side should have any interest in an escalation.

We consider the second aspect to be more problematic. The new elections in France have drawn investors' attention to the deficits in the budgets of many large industrialized countries. Since 2019, the budget situation in many countries - France, Italy, the UK and, above all, the US - has deteriorated drastically. Much of the growth success there compared to Germany, which has a much more solid budget, has been bought on credit. At just under 100 percent of GDP in the USA and UK, 110 percent in France and 140 percent in Italy, this ratio has reached new record levels. A period of austerity would actually be necessary now. However, the French election shows us that this will simply not be possible.

A quick look at the two-tier French electoral system shows that this will not be possible: In the past, this ensured that the extreme parties lost ground in the second round. Today - at least this is what polls suggest - the center is likely to be eliminated. Both extreme camps, the right and the left, are likely to make gains. And both are outdoing each other in promises to spend money like crazy and simply ignore the European Stability Pact.

Government deficits, in our experience, do not matter. Until the bond markets decide that they do matter. The elections in France and the UK at the beginning of July and in the US in November may bring us closer to this point. If bond yields were then to rise, the economy, the capital markets and probably also the central banks would have a real problem.

But we are not there yet. The positive assessment of the private wealth stock market indicator for the German stock market, which has been valid since October, has only suffered a slight initial setback. Overall, however, the economic indicator is still "green". Only three consecutive declines in the index for business expectations in the manufacturing sector would change this.

In addition to the economic development, the difference between current prices and the fair value of the DAX calculated by the editorial team is the second important criterion for determining the strategic corridor for the share allocation in the portfolio. The DAX currently stands at around 110% of its fair value. This is not cheap, but in itself is no reason to be pessimistic.

Nevertheless, due to the political situation, we are calling for more caution and are therefore paying more attention to the third part of the private wealth stock market indicator: the results of the capital market seismograph.

As you know, the seismograph distils the probabilities of three market states in the coming month from various variables - leading economic indicators, interest rate trends and price fluctuations on the stock markets. Green stands for the expectation of a calm, positive market. If green dominates, investors should invest in shares. Yellow indicates the probability of a turbulent, positive market - investing, but with a sense of proportion. And red indicates the probability of a turbulent-negative market. In this case, abstinence from equity investments is the order of the day.

The probability landscape of the seismograph has been stable and positive for some time. Currently, the probability of a positive, calm market continues to dominate. The probability of negative turbulence remains negligible despite the political irritations. For this reason, the seismograph still considers an offensive equity positioning to be appropriate. However, we will be monitoring this with increased attention in the coming days.

The bottom line for equity investors:

All components of the private wealth stock market indicator are still in the green. The strategic corridor for the equity allocation therefore remains at 70 to 110 per cent of the individually planned equity allocation. As the seismograph is also positive, the overall equity allocation is at the upper end of the strategic corridor - i.e. 110 per cent of the individually planned equity allocation.

This means that anyone who, for example, considers an equity allocation of 50 per cent to be optimal based on their individual preferences in the strategic asset allocation should currently be 55 per cent invested in equities (110 per cent of 50 per cent results in an equity allocation of 55 per cent).

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided on the private wealth website is for information purposes only and does not constitute an invitation to buy or sell securities.