Industrial economy may have bottomed out - continue to invest in equities.

The stabilisation process of the German economy is almost textbook. According to the ifo Business Climate Index, the situation has deteriorated continuously since mid-2022 and has now reached a level in February 2024 where positive and negative reports from the boardrooms roughly balance each other out. That looks like zero growth. Will it stay that way in 2024? Will the economy improve in future? Or will it continue to deteriorate? The business expectations for the next six months provide an insight into this. Although these are still pessimistic, the degree of scepticism is slowly decreasing. The ifo therefore writes that the economy is stabilising at a low level.

In our view, there is even justified hope that this could result in a slight upward trend as the year progresses. Firstly, the global economy is performing better than expected. Positive economic surprises are increasing around the globe. According to the OECD's leading economic indicator, 71 per cent of the countries surveyed saw an improvement in the economic situation in December compared to the previous month, with China and the UK showing the strongest increase. This is of great importance for the export-dependent German economy. Secondly, the government - shocked that it had to drastically cut its overly positive growth forecast for 2024 - has now also recognised the need to do something for growth and competitiveness. Only the way forward is still being debated. And thirdly, the falling inflation rate is significantly improving the outlook for private consumption. In view of the recent very significant wage increases, real purchasing power should rise sharply in 2024. This will support consumption.

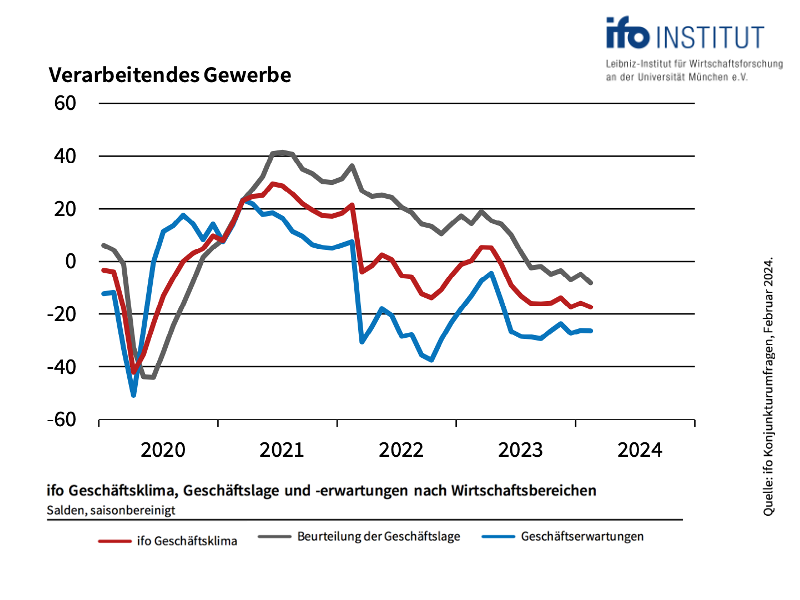

The assessment outlined above for the economy as a whole also applies in principle to industry. Although the situation is poor, business expectations, which are decisive for the private wealth stock market indicator, are stabilising. The ifo Institute's February survey shows: Expectations for the next six months remain at the low level of January, but at least they did not deteriorate any further (chart). This means that the positive economic signal from the end of November 2023 is still valid for the private wealth stock market indicator.

The bottom line for equity investors:

All three components of the private wealth stock market indicator continue to look promising.

The economic indicator has been "green" since November 2023 because ifo business expectations in industry improved three times in a row after a long, continuous decline.

The current market valuation of the DAX relative to its long-term calculated value is slightly above its fair value following the price increase in recent weeks. However, this is not yet a cause for concern and does not trigger a reduction in the equity allocation. The strategic corridor for the equity allocation therefore remains at 70 to 110 per cent of the individually planned equity allocation.

Nevertheless, we would like to point out that valuations have been much more favourable in similar economic phases in the past. If the thesis of an economic turnaround proves to be wrong, the DAX would have significant correction potential. In this context, it is interesting to note that many small and medium-sized companies have now become very cheap. Their valuation is much better suited to the current situation. This is also where the greater potential lies should the economic turnaround become a reality.

Within this range of 70 to 110 per cent of the individually planned equity allocation, the results of the capital market seismograph determine the exact positioning of the stock market indicator. The seismograph combines various variables - leading economic indicators, interest rate trends and price fluctuations on the stock markets. The probabilities for three market states in the coming month are distilled from this. Green stands for the expectation of a calm, positive market. If green dominates, investors should invest in shares. Yellow indicates the probability of a turbulent, positive market - investing, but with a sense of proportion. And red indicates the probability of a turbulent-negative market. Then abstinence from equity investments is the order of the day.

"For some time now, the probability landscape of the seismograph has been stably positive," reports Oliver Schlick, Secaro, who regularly calculates the current status of the seismograph: "The probabilities for a positive, calm market dominate, the probability for negative turbulence is negligible. Specifically, the seismograph considers an offensive equity positioning to be appropriate."

The overall equity allocation of the private wealth stock market indicator remains at 110 per cent of the individually planned equity allocation. This means that anyone who considers an equity allocation of 50 per cent to be optimal based on their individual preferences in the strategic allocation of assets should be 55 per cent invested in equities (110 per cent of 50 per cent results in an equity allocation of 55 per cent).

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided on the private wealth website is for information purposes only and does not constitute an invitation to buy or sell securities.