Buy signal confirmed.

A month ago - at around 14,800 points in the DAX and 23,800 points in the MDAX - we wrote here:

"A good acquaintance once said: the worse an investment feels at the moment you buy it, the better its long-term prospects. Voilà. Here we are. It actually feels very bad to invest more heavily in German equities right now. The "sick man of Europe" is in recession, the DAX has been trending downwards for weeks and the shares of small and medium-sized companies in particular have fallen massively in value. Nevertheless, the private wealth stock market indicator is giving an initial buy signal. The specific equity allocation suggested by the stock market indicator will be increased to 100 per cent of the individually planned equity allocation."

You can read the reasoning here (link).

Today, the German stock market is trading around 10 per cent higher. And the results of the ifo survey on the business climate in November have confirmed the buy signal.

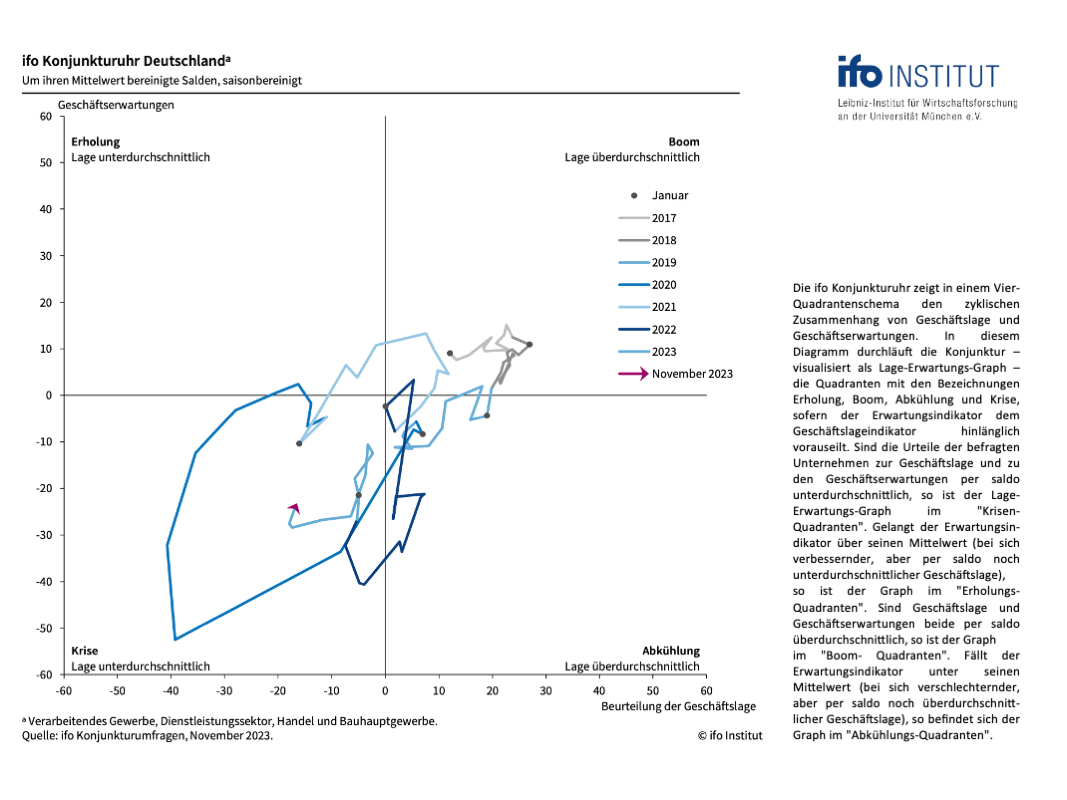

As you know: In the past, surveys by the Munich-based ifo Institute on business expectations in industry have proved to be an accurate leading indicator for the German stock market. The rule is: if business expectations improve three times in a row after a sustained decline, the economic component of the private wealth stock market indicator switches from "red" to "green". In the past, such an event often marked the start of the long journey from the crisis quadrant via the upswing quadrant to the boom quadrant on the ifo economic clock (chart 1). This was always a very lucrative journey for equity investors.

The basic idea: if business expectations improve after an economic downturn, the news from the boardrooms gradually becomes less pessimistic. Profit forecasts are initially no longer revised downwards and then become more optimistic again in the next stage. The foundations have been laid for a new upswing on the stock markets.

The time series on business expectations in industry had already suggested this trend reversal at the end of October. In the ifo Institute's monthly survey, participants can choose between three possible answers: They expect their business to be either "more favourable", "unchanged" or "less favourable" over the next six months. The balance of the business expectations published by the ifo Institute is calculated from the difference between the percentages of "more favourable" and "less favourable" answers.

A month ago, the data series read as follows: Continuous decline from April to July 2023 to a level of minus 29.6. The index then remained at minus 29.6 points in August and finally rose slightly to 29.5 points in September. In October, the index then improved significantly from minus 29.5 to minus 26.5 points.

Strictly speaking, the third increase in business expectations was still missing for a flawless economic buy signal. Until then, there had only been a sideways movement and two improvements. Nevertheless, in our view it seemed justified to become a little more aggressive in our equity investments at the end of October.

With the ifo surveys in November, this - we expected - third consecutive increase has now become a reality. The ifo business expectations in industry improved further to just minus 23.1 points. "Companies' scepticism for the coming months has decreased noticeably," commented the Munich-based economic researchers.

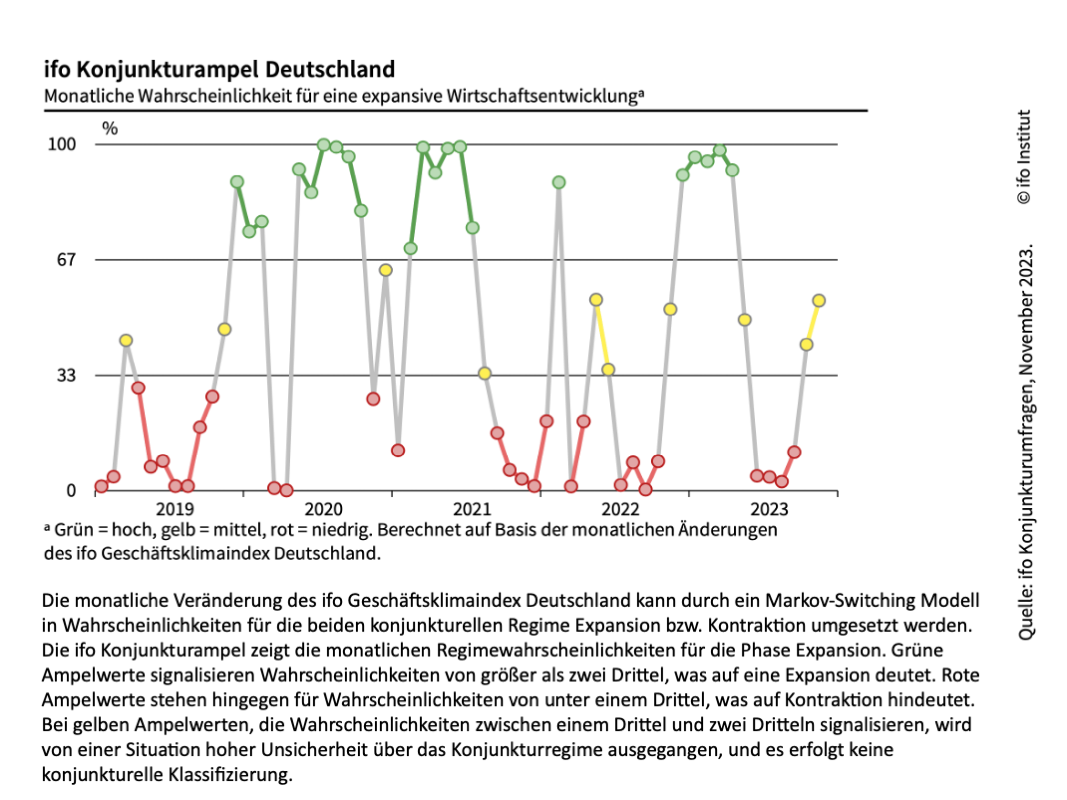

Although the ifo Business Cycle Clock is still in the crisis quadrant, it is now clearly pointing towards recovery (Chart 1). And the ifo economic traffic light is at least showing amber again (chart 2).

This is typical of a lower economic turning point and good news for equity investors. If the economy continues to stabilise in the coming months, small and medium-sized stocks in particular should benefit. They had suffered particularly badly until the buy signal at the end of October and are still undervalued according to our models.

One small fly in the ointment: the second leg of the stock market indicator - the relationship between the current valuation of the stock market and its medium-term "fair value" - has deteriorated somewhat due to the rapid rise in share prices over the past month.

The DAX is currently trading close to its fair value again. Despite the confirmation of the economic buy signal, it is therefore only sufficient to slightly increase the strategic corridor for the individually planned equity allocation.

The private-wealth stock market indicator is increasing the corridor from the current 60 to 100 to 70 to 110 per cent (if share prices had not risen since the end of October, the stock market indicator would have suggested a corridor of between 75 and 115 per cent).

Within this range, the results of the capital market seismograph determine the exact positioning of the stock market indicator.

The seismograph combines various variables - leading economic indicators, interest rate trends and price fluctuations on the stock markets. The probabilities for three market states in the coming month are distilled from this. Green stands for the expectation of a calm, positive market. If green dominates, investors should invest in shares. Yellow indicates the probability of a turbulent, positive market - investing, but with a sense of proportion. And red indicates the probability of a turbulent-negative market. In this case, abstinence from equity investments is the order of the day.

The probability landscape of the seismograph has been stable positive for some time. The probabilities for a positive, calm market and for a positive-turbulent market are well above 90 per cent overall. The probability of negative turbulence is negligible. Consequently, the seismograph considers a full investment to be appropriate.

The conclusion:

All three components of the private wealth stock market indicator continue to look promising. The economic trend in Germany gives a clear buy signal. The current market valuation of the DAX relative to its long-term calculated value is still fair. The combination of these two factors increases the strategic corridor for the equity component from the current 60 to 100 per cent to 70 to 110 per cent.

In view of the full investment ratio suggested by the capital market seismograph, the equity allocation suggested by the stock market indicator therefore increases to 110 per cent of the individually planned equity allocation.

In concrete terms, this means that anyone who considers an equity allocation of 50 per cent to be optimal based on their individual preferences in the strategic asset allocation should now not only fully utilise this allocation. As announced a month ago, equities are now even overweighted in the model (110 per cent of 50 per cent results in an equity allocation of 55 per cent in this case). It should be particularly worthwhile to consider small and medium-sized stocks.

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided on the private wealth website is for information purposes only and does not constitute an invitation to buy or sell securities.