Good news from the economy.

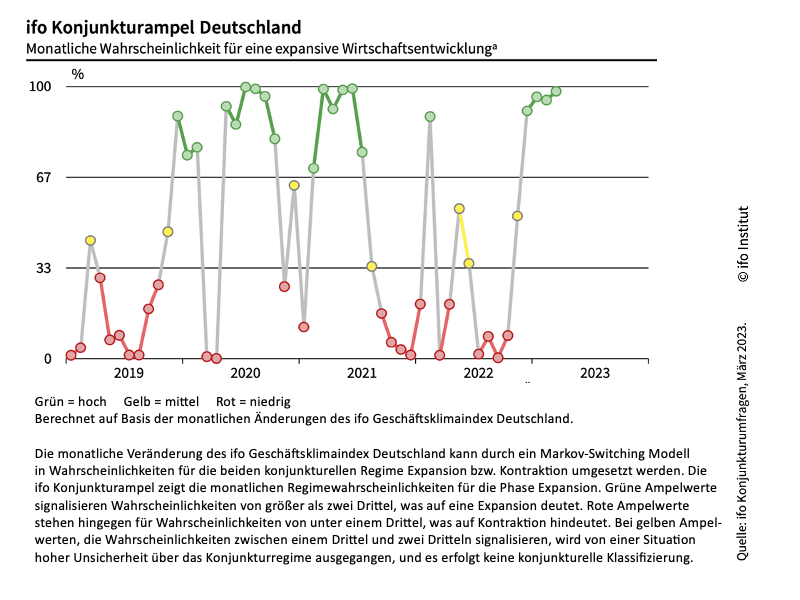

Situation better, expectations more optimistic - the Ifo Business Climate in March puts a tick behind the recession fears in Germany. The positioning on the ifo business cycle clock continues to move steadily in the direction of recovery (chart above). And the economic traffic light of the Munich-based economic researchers is green (bottom chart).

The index for business expectations in industry, which plays a decisive role in the private-wealth stock market indicator, has recovered particularly dramatically recently. It climbed steadily from minus 40.5 points in October 2022 to just minus 5.1 points (chart below). In plain language: the number of those who expect their business to improve over the next six months is now almost as large as the number who expect it to worsen. Particularly in key sectors such as the automotive industry, chemicals, electrical engineering and mechanical engineering, writes the ifo Institute, sentiment improved significantly.

Another positive development is that new orders in industry have also risen significantly in the past two months, see chart above. We pointed out here at the beginning of February that a recovery in this statistic was urgently needed to underpin the budding optimism in the boardrooms.

Now that this has occurred, the economic trend further solidifies the strategic buy signal for German equities in the January 2023 private-wealth stock market indicator.

So is all well for equity investors?

Not quite. Because while the current data from the real economy means tailwind for equity investments, there is still headwind from the monetary sector. Even before the banking quake, financial institutions had tightened the conditions for lending. According to data from the British research house Capital Economics, net lending to the private sector has fallen in three of the last five months. This is very unusual and, taken in isolation, raises fears of another dampening of economic activity in the medium term.

With the turmoil surrounding Crédit Suisse and Silicon Valley Bank, financing conditions have now tightened even further. Not for nothing did US Federal Reserve Chairman Powell remark that this was worth "an interest rate hike or maybe more".

So it remains exciting. The opposing development of real economic and monetary factors will probably continue to cause major fluctuations on the stock markets. We continue to assume a stock-picker market with a positive underlying trend.

The bottom line:

The economic component of the private-wealth stock market indicator remains positive. The DAX is currently trading at slightly more than 90 percent of its fair value and is thus slightly undervalued. In sum, these two components result in a strategic corridor of between 65 and 95 percent of the individually envisaged equity allocation for the proposed equity ratio.

Within this corridor, the results of the capital market seismograph define the exact equity quota. The probability landscape of the seismograph has been dominated by the negative turbulence probability (red) for some time, which suggests a cautious investment strategy. "The situation remains turbulent. However, since the probability of a positively turbulent market (yellow) has recently increased again somewhat, the seismograph is now positioned somewhat less defensively than it was a month ago," informs Oliver Schlick, who translates the seismograph's signals into allocation proposals for Secaro GmbH.

Therefore, the equity allocation suggested by the private-wealth stock market indicator has recently moved slightly away from the lower edge of the strategic corridor and now stands at 74 percent of the individually envisaged equity allocation. Given the challenging overall situation outlined above, we feel very comfortable with this allocation. The model is invested, but still has cash to take advantage of possible turbulence.

The reference to the individually intended share of equities is very important to us in this context. Models like the private-wealth stock market indicator can only ever be based on economic data. How high the individual equity quota should be in times of war is something each investor must decide on the basis of his or her own risk appetite and risk-bearing capacity.

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided in private wealth is for informational purposes and is not an invitation to buy or sell securities.

For a more detailed explanation of the private wealth stock market indicator, please read "News from the editorial office - strategic buy signal for German stocks" of 25 January 2023.