Strategic buy signal for German equities.

The economic component of the private-wealth stock market indicator provides a strategic, long-term buy signal for German equities. It is therefore advisable to increase the equity ratio.

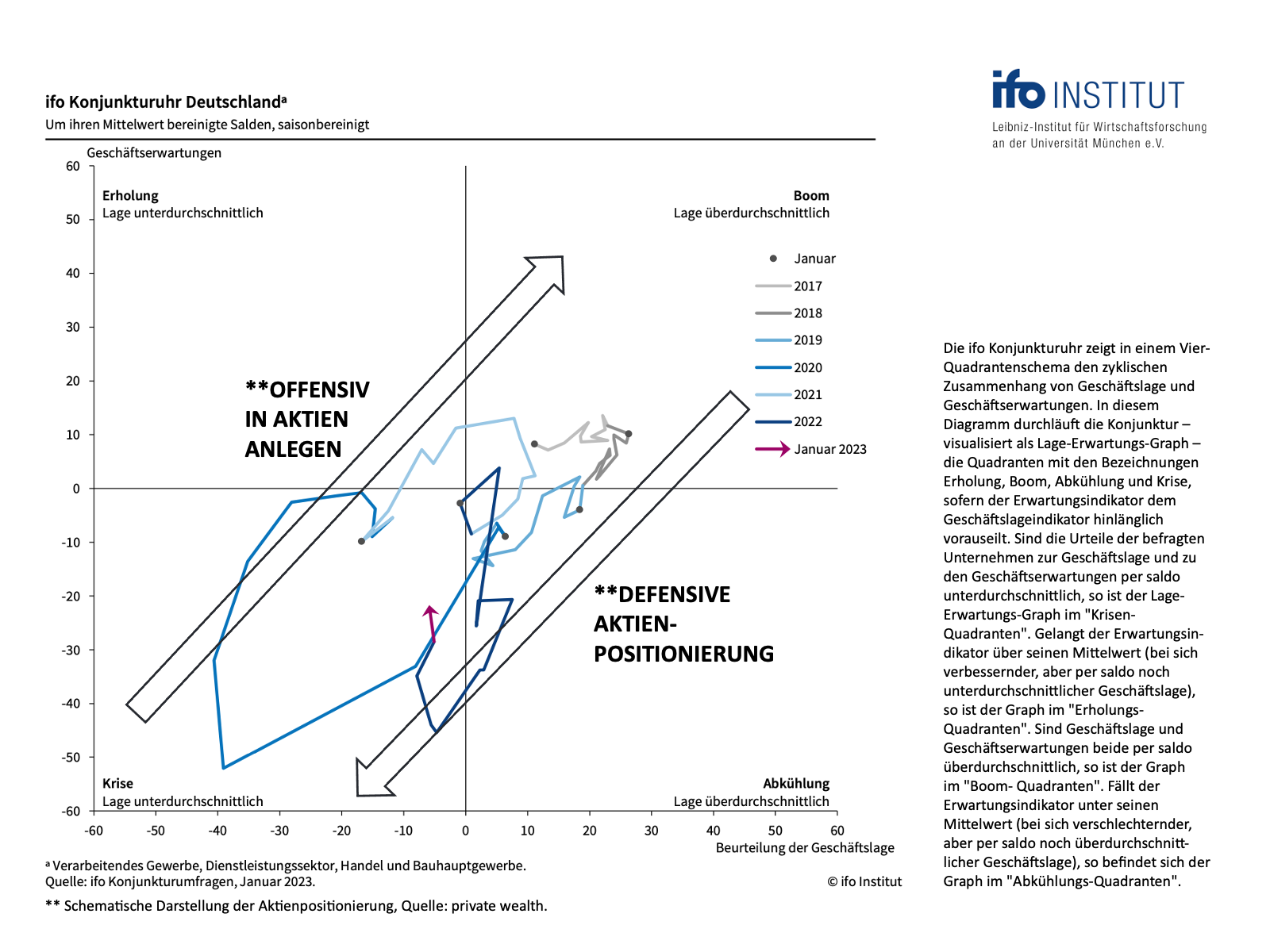

You know: The equity allocation corridor suggested by the private-wealth stock market indicator is determined by two factors - the economic trend and the valuation of the DAX. Basically, it is about being strategically more invested in equities when the DAX is low and the German economic traffic light is green at the same time. This means that the risk-reward ratio for equity investments is favourable. If the economic outlook deteriorates and/or equities are highly valued, the stock market indicator gradually goes on the defensive.

The private-wealth stock market indicator is therefore not designed to accurately predict trend reversals on the stock markets. The aim is to largely follow the long-term upward movements on the stock markets and to avoid the major downturns for the most part.

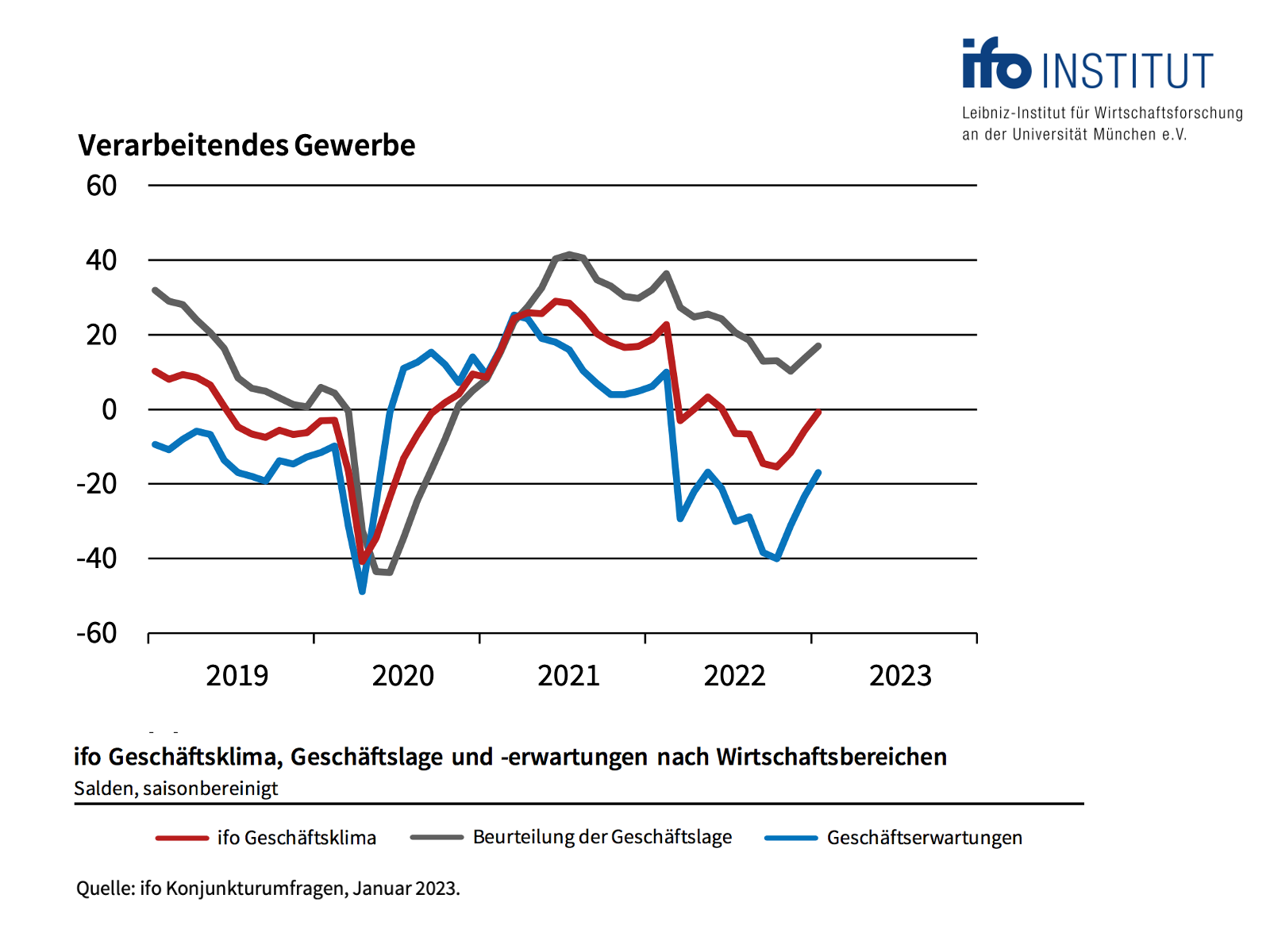

The decisive role in the analysis of the economic trend is played by the monthly survey of the ifo Institute on the business climate in Germany. 9000 entrepreneurs are asked about their business expectations for the coming six months. They have the choice between three answer options: "more favourable", "unchanged" or "less favourable".

The balance value of the business expectations published by the ifo Institute is the difference between the percentages of the answers "more favourable" and "less favourable". If this indicator improves three times in a row in industry after a sustained decline, this has very often been the signal for a turnaround in industry in the past. At this moment, the business cycle component of the private-wealth stock market indicator therefore switches from "red" to "green".

This is exactly what happened with the Ifo business survey in January. Business expectations in industry had declined continuously from February 2022 to October 2022. In November, December and now also in January, an increase was recorded again. The index climbed from minus 40.1 points in October to minus 31.1 and minus 23.4 to now only minus 16.9 points. In the past, a similar comeback was only observed in 2020 after the Corona slump and in 2009 after the financial crisis.

This is remarkable: only a few weeks ago, a recession in Europe and Germany was considered a foregone conclusion. Now it looks like we might get off lightly. The recent, dramatic drop in electricity and gas prices to the level before Russia's invasion of Ukraine is easing the burden on households and businesses alike. At the same time, supply chains are functioning better again. The order backlog in industry, which according to the ifo Institute remains at a high level, can now be worked off. And last but not least, the second most important player in the global economic concert - China - has switched back to expansion. All this could carry German industry through a possible phase of economic weakness in the coming months.

For equity investors with a long-term time horizon, this is good news. In the past, it was always successful to be invested in equities when the economy moved from the crisis sector via the recovery into the boom quadrant on the ifo economic clock. The beginning of this has now been made.

In the short term, however, things could still get turbulent on the stock markets. After all, it is very unusual to signal the end of an economic downturn before it has even really begun. Normally, such a constellation arises in the middle of a recession. Have we really reached that point yet? Or will the massive interest rate hikes by the central banks cause another economic setback? We will be watching this closely for you.

The valuation of the market plays an important role in answering the question of how much the equity ratio should currently be increased. The basic concept was outlined long ago by the great investor André Kostolany. He compared the interaction between the economy and the stock market to the walk of a dog with its master. While the man - the economy - moves slowly and steadily forward, the dog - the stock market - sometimes runs ahead. Or stays behind. At some point, however, he always comes back to a master.

The fair value model of private-wealth reflects the path of the economy, i.e. the path of the master. The comparison with the current quotations shows how far the dog has run ahead or fallen behind. Currently, the DAX is holding at just over 90 percent of its fair value. So while it is not extremely cheap, it is still slightly undervalued.

Together, the valuation and economic components define the strategic corridor for the equity ratio suggested by the private wealth stock market indicator. Up to now, this has been between 45 and 75 percent of the individual portfolio share earmarked for equity investments. After the buy signal of the economic indicator, the corridor will be raised to 65 and 95 percent. In plain language: 65 to 95 percent of the portfolio share individually earmarked for equity investments should now be invested.

Within this corridor, the capital market seismograph decides on the exact allocation. As you know, the seismograph combines various economic variables, some of which are updated on a daily basis - early economic indicators, interest rate developments or price fluctuations on the stock markets.

From these, the probabilities for three market states in the next month are distilled. Green stands for the expectation of a calm, positive market. If green dominates, investors should invest in shares. Yellow indicates the probability of a turbulent positive market - invest, but with a sense of proportion. And red indicates the probability of a turbulent-negative market. Then abstinence from equity investments is the order of the day

The seismograph has been positioned defensively for some time. And unlike the ifo business climate, the seismograph is not giving the all-clear even now. "The data from the USA are particularly critical," informs Oliver Schlick, who translates the signals of the seismograph into allocation proposals for Secaro GmbH, "both retail sales and industrial production are tending towards weakness and show that the dangers of recession have rather intensified in the USA recently. At the same time, the labour market remains solid. Because core inflation is therefore likely to remain stubbornly high thanks to higher wages, hopes that the US Federal Reserve might flatten the path of its interest rate hikes are premature. Whether market expectations of only a 0.25 per cent rate hike in February will be realised is open to doubt." The overall probability landscape of the seismograph, Schlick said, is therefore still dominated by the negative turbulence probability (red). "This suggests that we should remain cautious," says Schlick.

The bottom line: for the private-wealth stock market indicator, the defensive stance of the seismograph means keeping the equity exposure in the lower range of the strategic corridor of 65 to 95 per cent. The stock ratio specifically suggested by the stock market indicator therefore increases by 20 percentage points from 50 to 70 percent of the individually envisaged stock ratio. Part of the capital parked in cash so far should now be invested.

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided in private wealth is for informational purposes and is not an invitation to buy or sell securities.