The ifo climate crashes on schedule.

A month ago, we wrote in this space: In our view, it is very likely that an overwhelming majority of the entrepreneurs surveyed by the ifo Institute in March will assess their business expectations less favorably on a six-month horizon. In this case, the expectations component in the ifo climate would decline significantly - and not gradually, as in a normal business cycle, but quickly and abruptly.

At the time, we simulated how the private-wealth stock market indicator would react to such a development and reduced the equity allocation to a range between 45 and 75 percent of the individually intended equity allocation.

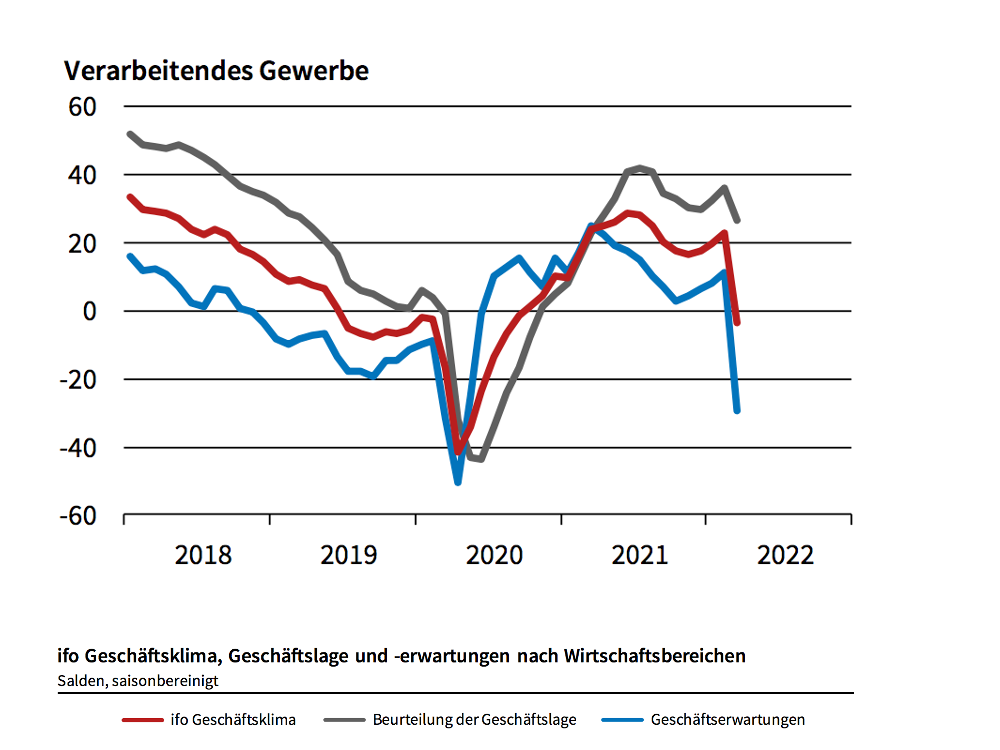

What we feared a month ago has now come true. The ifo Institute reported a "historic" slump in business expectations late last week. In the industrial sector, this index has fallen more than ever (chart above). The reaction of most commentators is now: recession ante portas.

We are not so sure.

For your information: as part of its monthly survey, the ifo Institute asks companies to report whether they expect business to develop "more favorably", "steadily" or "less favorably" over a six-month horizon. The balance of business expectations is then calculated as the difference between the percentages of "more favorable" and "less favorable" responses.

That a clear majority would assess future development "less favorably" in view of the war and the massive uncertainties is no surprise.

However, this says nothing about how big the dampener for the economy will be in absolute terms.

The ifo Institute itself has just published a new economic forecast on this. The researchers point to two opposing factors:

On the positive side, they say, order books in industry are fuller than they have been for years. In addition, private consumption could experience a boost in the coming months. After all, sales in many contact-intensive sectors are still low. In view of the easing and a possible improvement in the Corona situation in the summer, there is catch-up potential here.

On the negative side, the progress and consequences of the war are completely incalculable. The purely economic extent of the upheavals depends above all on the further course of commodity prices and the reactions of consumers and entrepreneurs. Will they curtail their purchases of durable consumer goods and their investments in view of the massive uncertainties?

Because this is difficult to calculate, the Munich-based economic researchers worked with two scenarios. In the base scenario, it is assumed that raw material prices have peaked and that supply bottlenecks and uncertainty will now decline in perspective. The German economy is then expected to grow by an impressive 3.1 percent in 2022. In the alternative scenario - assuming that raw material prices do not peak until the middle of the year and that uncertainties initially intensify - growth of 2.2 percent is still on the cards.

That is encouraging.

However, the ifo Institute does make one reservation. The effects of an energy embargo against Russia are not included in the scenarios. In this case, the experts say, the damage would be "far greater." The probability of a recession would then be "high."

The range of possibilities for future economic development is therefore broader than ever before. What is important for investors is that in the event of a significant weakening of economic momentum or even a recession, a massive reduction in earnings forecasts for cyclically sensitive companies would have to be expected. The decisive factor will then be whether the angers - as after the corona shock in the summer of 2020 - are prepared to look across this valley. That is not yet foreseeable today. A defensive stance toward equity investments is therefore still appropriate.

The bottom line:

Since February 28, the private wealth stock market indicator has been positioned defensively. It provides a corridor for the recommended equity allocation of between 45 and 75 percent.

Within this range, we are guided by the results of the capital market seismograph. As the latter currently indicates a maximum underweight, the equity allocation suggested by the private wealth stock market indicator remains at 45 percent of the individually envisaged equity allocation.

We expect the next data from the seismograph shortly. Please leave your mail address at www.private-wealth.de or register with your mail address for a free six-month trial subscription. Only then we will be able to send you a "private-wealth-alert" immediately.

Sincerely,

Yours

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be assumed for the accuracy of the content. The information provided in private wealth is for informational purposes and is not an invitation to buy or sell securities.