Orientation. In the eye of the storm.

Strategy. How will the global economy develop? How will corporate earnings turn out in the future? Which losses at companies will be temporary, which permanent? And how should investors position themselves now? The Lerbach Competence Circle, an illustrious panel of 26 family officers, asset managers and private bankers, has answers to the most important questions from investors.

Strategy. How will the global economy develop? How will corporate earnings turn out in the future? Which losses at companies will be temporary, which permanent? And how should investors position themselves now? The Lerbach Competence Circle, an illustrious panel of 26 family officers, asset managers and private bankers, has answers to the most important questions from investors.

If a hurricane turns fast enough, an eye can form. Inside it is cloud-free and almost windless.

In recent weeks, many an investment professional rubbed his eyes in amazement. Economic researchers wrote in negative superlatives - the worst, worst, deepest, biggest, most severe slump since the Second World War is looming. An economic tornado. And on the stock markets? Stock prices rose. Most indices have now recovered much of their losses from the Corona crash. Anyone who spent the last six months on a desert island would diagnose a normal correction. Crisis? What crisis?

"It's not as irrational as it may seem at first glance," explains Marco Willner, NN Investment Partners, "at the moment two giant powers are working in exactly opposite directions. It's like a gigantic tug-of-war. And currently, those who see the glass half full have the upper hand."

The most important argument of the optimists is the enormous liquidity. All central banks are flooding the financial system with their bond purchases. The total global monetary stimulus is around nine trillion dollars. The unit of account has long since changed. The trillion is the new billion.

"In addition, many investors sold in the crash and are now looking to re-enter the market," observes Bernd Meyer, Berenberg. "4.8 trillion dollars are parked in money market funds, in the USA alone. By way of comparison, the total market capitalization of European equities is 3.5 trillion, that of emerging markets 4.9 trillion. This capital would therefore be enough to buy up all emerging market equities. As real interest rates become increasingly negative, some of this money will revert to equities, corporate bonds and precious metals."

And then there is the factor of hope. Research into corona drugs and vaccines is making progress. The end of the lockdown promotes the expectation of a rapid economic recovery. The basic thesis is that this recession is different. Because it was prescribed by the state, it can also be ended by decree. Until the economic engine is running smoothly again, major damage is to be prevented by massive government aid programmes.

According to estimates by the International Monetary Fund, global net new debt is therefore expected to account for almost ten percent of global value added by 2020. "That is around 14 trillion dollars or more than three times the German national product," explains Christian Jasperneite, M.M.Warburg. Another ten trillion in economic stimulus packages could be added in 2021.

"Money and fiscal policy are a powerful combination. And because the future is being traded on the stock market - the stock market is looking two years ahead on average - many people are already buying now," concludes Family Officer Kai-Arne Jordan and concludes: "The further prices rise, the greater the fear of missing something. There is even an acronym for this: Fomo - fear of missing out."

"This positioning can also be justified by theoretical models for share price valuation," adds Georg Graf von Wallwitz, Eyb & Wallwitz: "Imagine you are an entrepreneur. Every year you receive a cheque for the profit you have made. In 2020 this has now unfortunately been lost in the mail. Has this massively changed the value of your company? Certainly not."

"In principle, goodwill is the sum of all future discounted earnings. However, given not too high payout ratios and low interest rates, the future is much more important than the next six to twelve months," says Thomas Neukirch, HQ Trust, "We took a closer look at this based on historical profit data and current interest rate structure: If earnings were to be completely absent for twelve months, this would only reduce the value of the company by around ten percent. However, the prerequisite for this is that the company can then quickly build on its earlier successes.

This is precisely what those whose glass is half empty doubt. "The risk of a resurgence in contagion figures is incalculable," makes Carsten Mumm, Donner Reuschel, clear, "and the real economic data are catastrophic. In many areas, it will take a very long time before pre-crisis levels are reached again.

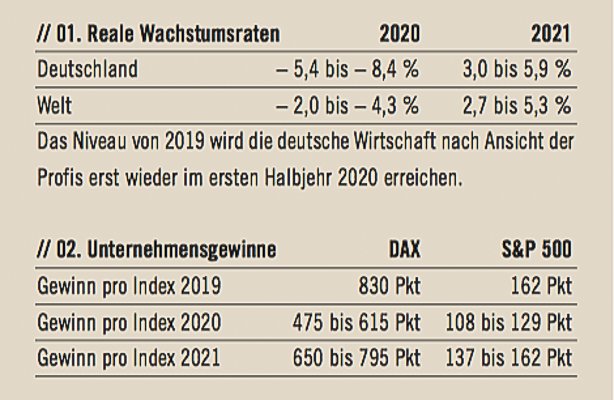

Despite the extreme measures of economic and monetary policy, the current situation is indeed dramatic. On balance, the Competence Group expects global economic output to fall by between two and 4.3 percent this year. In Germany, the experts forecast a decline of between 5.4 and 8.4 percent. The professionals assume that the economy will recover in 2021, but the level of 2019 will not be reached again until 2022. By comparison: In the year of the financial crisis, Germany recorded a minus of 4.7 percent, while the world got off with a minus of 1.7 percent.

"In Germany, ten million people are on short-time work, which is one third of the employment. The situation is similarly bad in all other large European countries. In the USA, more than 20 million people have registered as unemployed within two months. The unemployment rate already climbed from 4.4 to 14.7 percent. And FED boss Powell believes it is likely to rise further to 20 to 25 percent," Family Officer Joachim Meyer lists. "Just for comparison: The highest value during the financial crisis was reached by the initial applications for unemployment assistance in the USA in March 2009, at 665,000. That is many times worse today," adds Ulrich Voss, Tresono Family Office.

"Many market participants today rely exclusively on monetary policy. It does not matter to them how far the national product and earnings collapse, as long as there is an unlimited supply of liquidity", summarises Alexander Prochnow-Ast, Family Office - Volksbank Kraichgau, and concludes: "I do not believe that this calculation will work out".

He is not alone in this assessment. Just how cautious the Lerbach Competence Group has recently become is shown by the current positioning of the professionals on the stock market compared with the share of equities, which is considered strategically correct in the long term. None of the professionals is currently overweight in equities. Only 20 percent of the respondents are normally weighted. In contrast, 80 percent are underweight, in some cases significantly so. In total, the competence group currently holds eleven percent of the portfolio in cash and is waiting to invest this at 10 to 20 percent lower prices on the stock market. The group has never been so defensive before.

What could trigger another slide in share prices? "A second downward wave would first of all follow the typical pattern of the past. After each crash, there was initially a countermovement driven by hope. Then it turned out that the economic recovery is bumpier and takes longer. As a result, prices fell again more slowly, but significantly. This was the case during the recession from 2001 to 2003. And that was also the case in 2008/2009. I don't know why it should be different this time", explains Axel Angermann, FERI.

"With all the fantasy billions of states, it is just not possible to get an economy up and running again so quickly", Karsten Tripp, HSBC Germany, is convinced. Politicians often forget that. Money alone will not heal the wounds torn open by the destruction of billions of micro-supply and value-added chains" "Above all, the fact that the whole world is affected - to varying degrees - makes a comeback difficult," emphasizes Jörg Rahn, Wirtgen Invest. In India, 100 million jobs have been lost temporarily or permanently, the livelihoods of large sections of the population have been destroyed or are threatened with destruction. In Brazil, the danger of national bankruptcy is growing. Russia is suffering from the drop in oil prices. "And all countries with high value-added tourism sectors will have difficulty recovering. But these are important sales markets for German industry," adds Daniel Oyen, von Plettenberg, Conradt & Cie. family office.

"That's why I suspect that the second-round effects of the crisis will be severe," adds Alexander Prochnow-Ast. "This may have started as a recession decreed by the government. But in the future we will see the same mechanisms as in any other recession - unemployment and short-time work weaken consumption, reduced production leads to declining investment".

For Germany, the ifo employment barometer already suggests that short-time work will soon lead to redundancies. In industry, services and trade, the majority of the companies surveyed are planning to reduce their workforce in the next three months. "It will also be a disaster for the US economy, which is 70 percent dependent on consumption, if 30 to 40 million Americans become unemployed - even Amazon & Co. should feel the effects," Daniel Oyen continues. "The big wave of insolvencies is probably yet to come. Many companies have hardly any reserves and are now drawing down loans. In three to six months it will become critical," warns Alexander Ruis, SK Family Office. "And if massive amounts of loans were to default then, the banks would also be affected," adds Rahn.

All in all, according to the Competence Group, this is a mixed situation with very high risks, which simply does not fit in with the relaxed mood on the stock markets. "Especially the current earnings estimates traded at am Markt seem to me to be very, very optimistic", Thomas Buckard, MPF AG, reflects.

"The consensus of all analysts published by the data provider Factset expects the DAX to decline by 23 percent in 2020. For the S&P 500 it is only 19 percent", Christian Jasperneite informs. In contrast, the Lerbach-based competence group expects an average drop in profits of 35 percent for the DAX and 27 percent for the S&P 500.

Two observations are interesting. First, the experts give an enormous range. For example, they estimate a corridor between 475 and 615 points for DAX profits in 2020. That is enormous and shows how great the uncertainty is. "Secondly, even the cautious stance of the competence circle does not by a long shot reflect what we experienced in the recessions of 2001 and 2009, which were much less deep than what we must expect in 2020. At that time, profits collapsed by 40 to 60 percent," warns Jasperneite. That creates room for disappointment. "I don't trust the roast yet. There is a high probability that the earnings forecasts will be revised significantly further downwards in the coming months. When the full extent of the economic crisis is on the table, prices are likely to fall again," concludes Alexander Ruis.

The fact that the professionals in their sample portfolio for investors with average risk tolerance still hold 37 percent in shares needs explanation. "We are not a hedge fund that takes extreme bets", explains Stephan Jäggle, Münster Stegmaier Rombach Family Office, "our mission is to operate a balanced asset allocation that makes sense in the long term. Being even more defensive could not be justified in this respect.

In addition, it is important to maintain a balance between short-term caution and long-term optimism. "In the post-Corona era, equities will play an even more important role than today," Marc Vits of Bankhaus Metzler is convinced. "In fact, equities are likely to be one of the few asset classes in the next ten years with which earnings can be generated at all after inflation has been deducted. With most bonds, bank deposits or savings deposits, this is not possible," says Kai Röhrl. "The strategy must therefore really be to use the troughs of the coming wave movements for purchases," adds Ruis.

How do the professionals know that it's time to break cover? "It is important to orientate oneself more strongly than in the past to data that quantify changes in economic activity at very recent times," explains Jasperneite. For example, he uses statistics from the New York FED, which are updated twice a week. Or smartphone locations that show how the number of visitors in shopping malls changes.

We are in the eye of the storm: in the cloud-free, low-wind zone around the centre of rotation of an economic cyclone. If it continues to move, it is likely to cause further turbulence on the stock markets. According to the Lerbach Competence Group, investors should prepare themselves now. Because then it is important not to lose your nerve. But to buy with a view to the coming years.

____________________________________________________

Corporate bonds first?

"I have a chart there that I have been happy to show for a long time", says Stephan Jäggle: "The headline read "There's no more interest. In March, the "gibt" was replaced by "gab".

After the dramatic rise in yields on corporate and emerging market bonds, the interest rate segment has become interesting for investors for the first time in years. "I even suspect that the bond sector is recovering ahead of the equity markets," Karsten Tripp reflects. After all, in recessions, companies usually try to get their finances back in order. Balance sheet restructuring now takes precedence over profits, debt reduction over share buybacks. Creditor interests count more than the needs of shareholders.

"Of course there will also be insolvencies, coupon defaults. But that is precisely why the choice of securities is so crucial," Tripp makes clear and takes up the cudgels for active management. "Large companies will benefit more from government aid and are therefore less at risk of insolvency. And those with a functioning business model will probably even get rid of some competitors in the next few years. Investors don't get that differentiation when they use ETFs."

An opportunity could also arise from the structure of the market for corporate bonds. Many bonds today have a rating of BBB - the lowest rating in the investment grade sector, the area that is suitable for large institutional investors. "The recession is likely to result in numerous rating downgrades. If the bonds then fall outside the investment grade sector, ETFs that reflect this range, for example, will be forced to sell without limit. Those who are familiar with the respective companies and then collect these securities can benefit from this," Stephan Jäggle is convinced.

____________________________________________________

The forecasts of the competence circle.

How the Competence Group assesses economic and earnings development. And what portfolio allocation the professionals now advise.

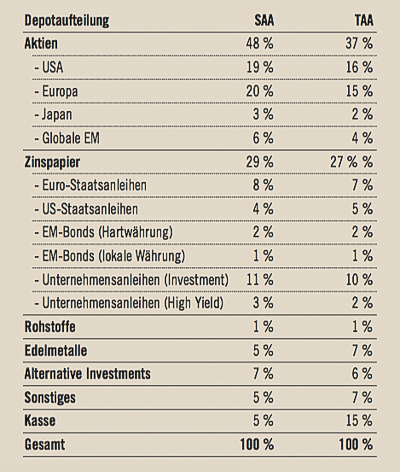

// 03. the experts' asset allocation

The table shows how the Lerbach Competence Circle would structure the liquid assets of an average investor willing to take risks. The comparison between the asset allocation (SAA) und considered strategically sensible in the long term with the current tactical quotas (TAA) illustriert the current positioning of the professionals.

At the moment, the experts are more cautious than ever before. They would invest the high cash proportion in shares at a level of 9200 Punkten in the DAX and 2470 points im S&P 500.

®

Author: Klaus Meitinger