Germany is turning the corner.

You will probably be startled by the headline "Germany in recession" in the next few days. This is because there is indeed a high probability that the German economy will have contracted slightly in the first quarter of 2024. The official definition of a recession - two negative quarters of GDP in a row - would then be fulfilled.

Don't be confused. That is the past. The economic low point should have been reached in February. This is indicated by the business climate survey conducted by the Munich-based ifo Institute. The mood among companies improved considerably in March. The current situation is now viewed more favourably than in the previous month. Above all, however, company bosses' expectations for the next six months were significantly less pessimistic than before.

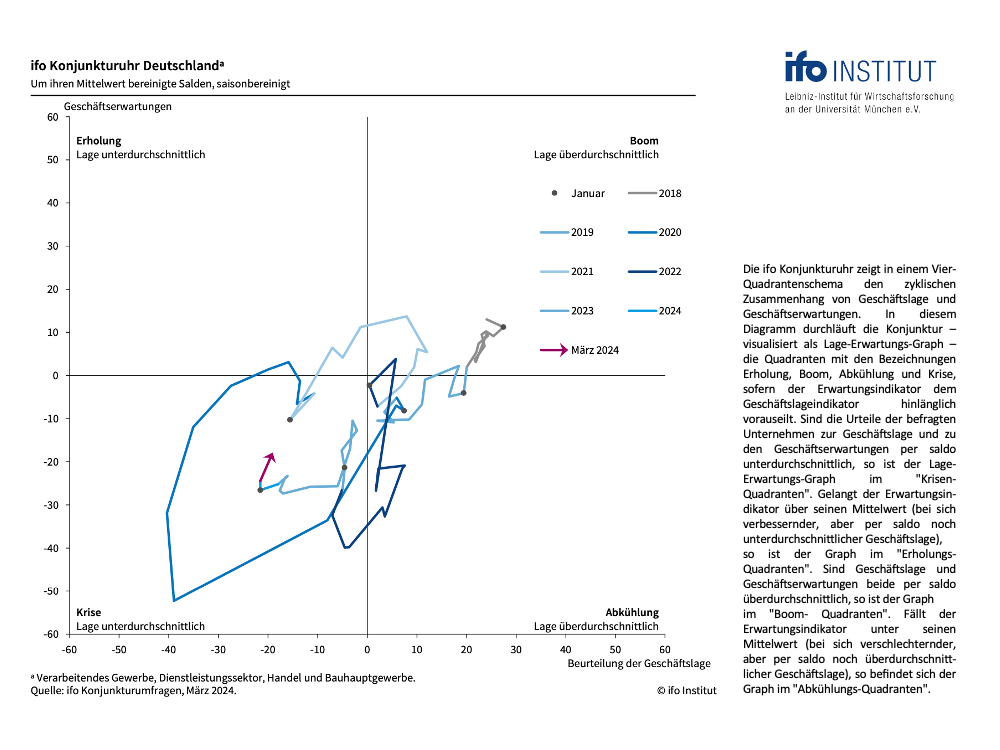

We already pointed out here a month ago that the stabilisation process of the German economy is proceeding almost textbook. This is impressively emphasised by the latest business climate data. The ifo economic traffic light has turned green (Figure 1). And the ifo economic clock has made a massive leap towards the recovery quadrant (chart 2).

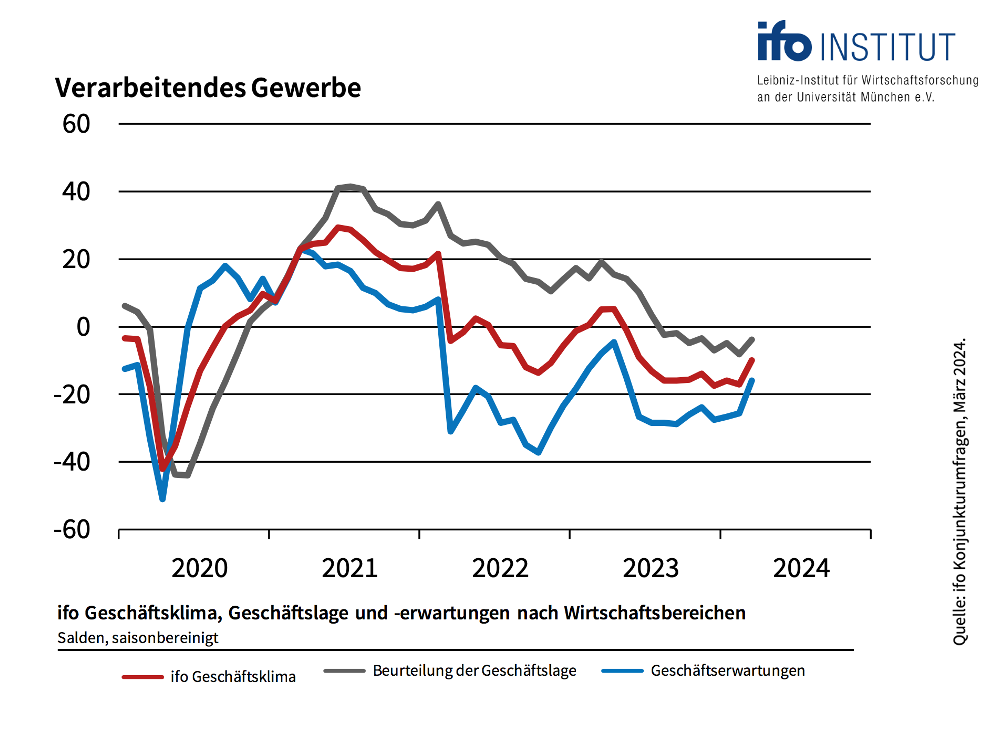

The trend reversal in industry, which is so important for the private wealth stock market indicator, is particularly impressive. The index for business expectations in the manufacturing sector made a big leap upwards (chart 3). It jumped from minus 25.6 to just minus 15.9 points. That is a huge improvement. We had already signalled the possibility of such a development a month ago and gave three reasons for this:

Firstly, the global economic outlook is predominantly positive. This is of great importance for the export-dependent German economy and is now also reflected in the ifo Institute's survey on sentiment in the export industry. Ifo export expectations recovered to minus 1.4 points in March (from minus 7.0 points in February). "Global trade is likely to pick up in the coming months. The German export industry hopes to benefit from this," comments Klaus Wohlrabe, Head of ifo Surveys.

Secondly, the German government has recognised the need to do something for growth and competitiveness. Although the extent of the growth promotion law that has just been passed is still far too small, at least the direction is right.

And thirdly, the declining inflation rate improves the outlook for private consumption. In view of the recent very high wage increases, people's real purchasing power should increase significantly in 2024. This will support consumption.

This development underlines the positive assessment of the private wealth stock market indicator for the German stock market, which has been valid since October. As a reminder: in October 2023, the stock market indicator gave a buy signal when the DAX fell below 15,000 points. At the time, the equity allocation was initially raised to 100% due to the stabilisation in business expectations. Since November, the stock market indicator has even been overweight in equities at 110 per cent.

The current constellation suggests that we should remain highly invested in equities. The path on the ifo economic clock from bottom left to top right has always been very lucrative for investors in the past. Rising sales and profits then generally drive share prices. This trend should even be supported by interest rate cuts by the central bank later this year.

The bottom line for equity investors:

All three components of the private wealth stock market indicator look promising.

The economic indicator has been "green" since November 2023. The current market valuation of the DAX relative to its long-term calculated value is slightly above its fair value following the price increase in recent weeks. However, the gap is not yet large enough to necessitate a reduction in the equity allocation.

The strategic corridor for the equity allocation in the private wealth stock market indicator therefore remains at 70 to 110 per cent of the individually planned equity allocation.

Within this range, the results of the capital market seismograph determine the exact positioning of the stock market indicator. As you know, the seismograph combines various variables - leading economic indicators, interest rate trends and price fluctuations on the stock markets. The probabilities for three market states in the coming month are distilled from this. Green stands for the expectation of a calm, positive market. If green dominates, investors should invest in shares. Yellow indicates the probability of a turbulent, positive market - investing, but with a sense of proportion. And red indicates the probability of a turbulent-negative market. In this case, abstinence from equity investments is the order of the day.

The probability landscape of the seismograph has been stable and positive for some time. The current calculation by Oliver Schlick, Secaro, also confirms the positive basic tone: "The probabilities for a positive, calm market dominate, the probability for negative turbulence is negligible. The seismograph therefore continues to consider an offensive equity positioning to be appropriate."

Overall, the equity allocation of the private wealth stock market indicator therefore remains at the upper end of the strategic corridor at 110 per cent of the individually planned equity allocation. This means that anyone who, for example, considers an equity allocation of 50 per cent to be optimal based on their individual preferences in the strategic asset allocation should currently be 55 per cent invested in equities (110 per cent of 50 per cent results in an equity allocation of 55 per cent).

Where will the favourites be found during the economic recovery?

Eduardo Mollo Cunha from Blackpoint Asset Management has provided us with an interesting analysis on this subject. Blackpoint determined the historically relevant factors during different economic phases in a global context. According to this analysis, the "valuation" factor, for example, only plays a subordinate role during the recession, but becomes the dominant criterion during the recovery. This is consistent with our observations in the German small and mid-cap segment. Shares in small and medium-sized companies have long been very favourable compared to the market as a whole. However, this has hardly aroused any interest among investors to date. On the contrary: these stocks have often become even cheaper. This could now change fundamentally in the recovery phase of the German economy.

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided on the private wealth website is for information purposes only and does not constitute an invitation to buy or sell securities.