Turnaround in the economy underpinned.

The emerging turnaround in the German economy is becoming increasingly clear. The German economy is more resilient than most economists had expected. This underpins the strategic buy signal for German equities from the business cycle component in last month's private-wealth stock market indicator.

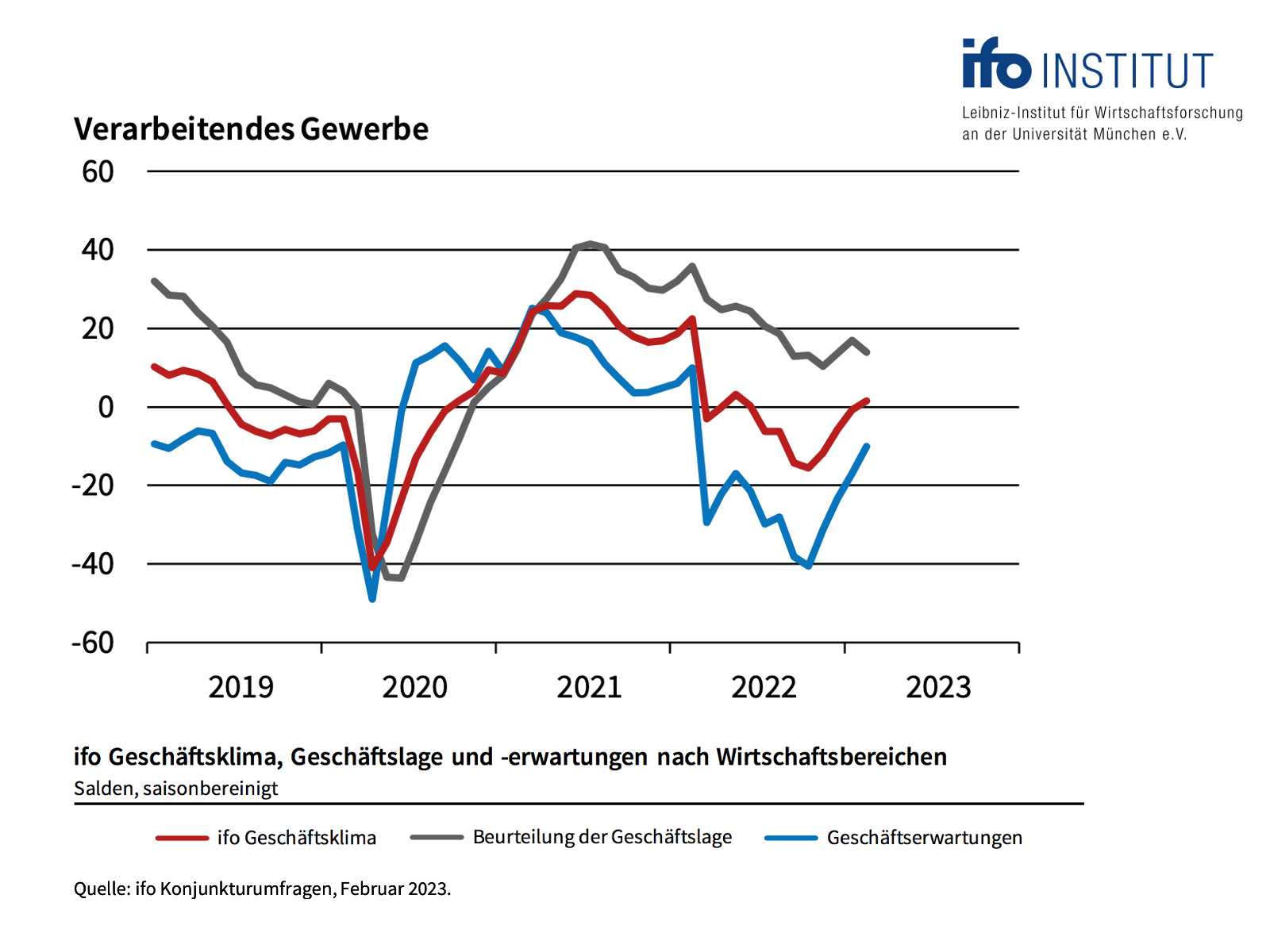

The latest ifo Business Climate Index for February shows a further improvement in sentiment in the German economy. The positioning on the ifo business cycle clock is now gradually moving in the direction of recovery (Chart above). And the economic traffic light of the Munich-based economists is also green.

This recovery is particularly significant for the index of business expectations in industry, which plays an important role in the private-wealth stock market indicator. The ifo Institute asks 9,000 entrepreneurs whether they assess their business outlook as "more favourable", "unchanged" or "less favourable" over a six-month period.

The published balance value is the difference between the percentages of the answers "more favourable" and "less favourable". This index climbed steadily from minus 40.5 points in October 2022 to only minus 10.1 points (Chart below). The number of those who expect an improvement is now almost as large as the number who expect a deterioration.

Several reasons are responsible for this brilliant comeback. For one thing, energy prices have fallen significantly, and concerns about an energy shortage have disappeared. Secondly, the opening of the Chinese economy after a long covid slump is encouraging. If the Chinese economy really were to pick up speed again in the future, German industry would benefit particularly strongly. Apparently, the corporate leaders surveyed are counting on this.

For equity investors, this is initially good news. For a long time, significant downward profit revisions had to be assumed for 2023 for many listed companies. It could be that these will only be much more moderate - if at all.

However, there is also a flip side to the coin. The more concerns about economic and corporate earnings fade into the background, the more prominently the issues of inflation, interest rates and central bank policy will return to the fore.

The current wage negotiations are clear evidence that inflationary pressures have solidified. Although inflation rates will fall significantly in March and April due to the base effects in energy prices. However, wage inflation and the scope for companies to pass on prices thanks to an improved economy will ensure that the dreaded wage-price spiral will continue to turn.

This increases the pressure on the ECB to raise interest rates more strongly and to remain on the monetary brakes longer than assumed. How this will then affect the fragile economic recovery in the longer term is an open question.

So it remains a challenging investment environment. Investors should expect tailwinds from the economy to meet stronger monetary headwinds in the coming weeks. We will therefore probably have to prepare for greater fluctuations in the equity markets.

The bottom line:

The economic component of the private wealth stock market indicator remains positive. The DAX is currently trading at around 95 percent of its fair value and is still slightly undervalued. In sum, these two components result in a strategic corridor of between 65 and 95 percent of the individually envisaged equity allocation for the proposed equity ratio.

Within this corridor, the results of the capital market seismograph define the exact equity quota. For some time now, the probability landscape of the seismograph has been clearly dominated by the negative turbulence probability (red), which suggests a cautious investment strategy. "In the seismograph, the variables derived from the interest rate landscape play a very important role. And these remain critical," explains Oliver Schlick, who translates the signals of the seismograph into allocation proposals for Secaro GmbH.

The private-wealth stock market indicator therefore suggests overall positioning near the lower edge of the strategic bandwidth. Specifically, the model advises an equity allocation of 70 percent of the individually intended equity share. Given the challenging overall situation outlined above, we feel very comfortable with this allocation. The model is invested, but still has cash to take advantage of potential turbulence.

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided in private wealth is for informational purposes and is not an invitation to buy or sell securities.

For a more detailed explanation of the private wealth stock market indicator, please read "News from the editorial office - strategic buy signal for German shares" of 25 January 2023.