Take profits.

The ifo business climate survey for July confirmed the downward trend in German industry. This means that one of the three factors of the private-wealth stock market indicator - the economic component - has turned red. Investors should reduce their equity exposure and take some profits.

The details: after peaking in February 2021, business expectations in the industrial sector have fallen for the fourth time in a row. In principle, the rule has applied in the past: if business expectations in the manufacturing sector fall three times in a row, this signals a trend reversal in the economy and provides a sell signal for equity investors. This is why profit-taking was actually already due four weeks ago. However, we deliberately refrained from doing so last month, as the concerns of industrial managers were mainly due to problems on the procurement side - supply bottlenecks or the resulting sharp rise in input prices. We saw this as a special situation and wanted to wait and see how the situation develops over the next month before changing our previously very offensive equity positioning.

However, the current decline in the expectations component (see chart 1) now signals that the difficulties apparently cannot be resolved so quickly. It would be negligent to ignore this. After all, the persistent supply bottlenecks could even lead to a renewed shutdown of production in the future. In the worst case, companies would then have to register for short-time work with full order books. Moreover, it could become difficult to pass on the higher input costs to sales prices. Profit margins would then suffer. Don't forget: investors' expectations in the equity markets regarding the rise in corporate profits in the coming quarters are now very high - if they were disappointed, the stock markets could suffer severe setbacks. The latest results from the ifo Institute now make this risk seem much greater.

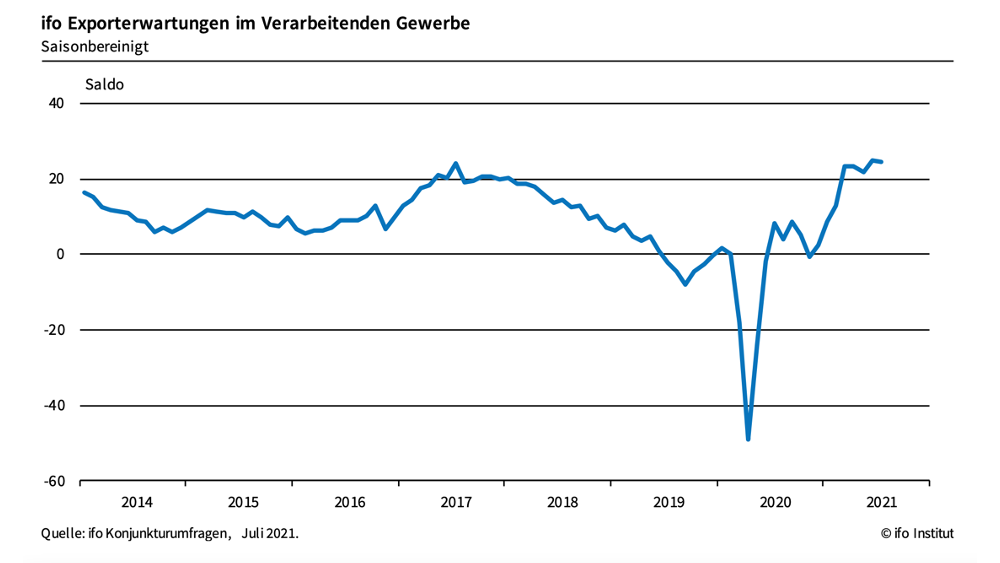

In addition: Following a stellar rise since November 2020, exporters' expectations regarding business developments in the coming three months now also appear to have peaked (chart 2). Against this backdrop, too, equity analysts' forecasts may perhaps be too optimistic with a view to the months ahead.

To determine how all this specifically affects the allocation of the private-wealth stock market indicator, we now need to take into account the other two components of the indicator - the current market valuation and the results of the capital market seismograph.

Our calculation of the fair value of the DAX is based on data material since 1954 and was adjusted a year ago to reflect the expectation that central banks will tolerate more growth and higher inflation rates without raising interest rates. Based on this assumption - which continues to be very plausible in our view - the German DAX is currently just below its fair value. From a valuation perspective, therefore, there is no reason to become pessimistic. The economic sell signal alone also only reduces the equity allocation to between 45 and 75 percent of the capital earmarked for equities (with a green economic traffic light, the corridor would be between 75 and 110 percent).

To determine the exact positioning within this corridor, we use the data from the capital market seismograph as an important third component, which Oliver Schlick, Managing Director of Secaro GmbH, regularly calculates and links to investment recommendations. "The seismograph remains positive, with a cumulative probability of a calm positive market (green) and a positive turbulent market (yellow) of around 99 percent. The probability for a turbulent negative market (red) still does not play a role at the moment", informs Schlick and further derives from this the recommendation "significant overweight".

For the private-wealth stock market indicator, this means that the very positive assessment of the seismograph lifts the suggested stock ratio to the upper edge of the corridor at 75 percent. Compared to the previous month, gains are nevertheless being taken in significant form. At that time, the ratio was finally at 110 percent.

So the private-wealth stock market indicator is taking its foot off the gas after a long period of overweighting in equities. However, if the downward trend in ifo business expectations were to reverse in the coming months, the model would also quickly become more offensive again. Until then, we remain cautious.

Have a relaxing summer,

Yours

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be assumed for the accuracy of the content. The information provided in private wealth is for information purposes only and does not constitute an invitation to buy or sell securities.