That's as good as it gets.

Dear Readers,

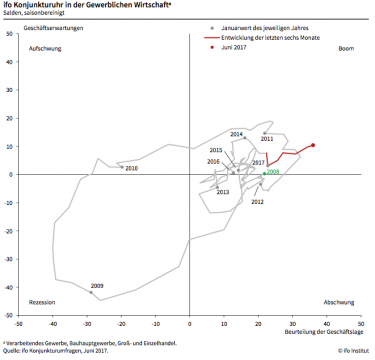

The ifo Institute reports new records in business climate, business situation and business expectations. "In the German executive floors," write the researchers themselves, "there is high spirits". A glance at the ifo economic clock shows that the German economy has never been so deep in boom territory before. It goes without saying that in this situation, the ifo traffic light will also keep to "dark green" (graphs below).

The boom in the German economy is progressing so briskly. Capacities are now being used at above-average rates almost everywhere. In the construction industry in particular, they are already very tense. In view of this boom, the insanity of a "one size fits all" monetary policy in Europe is once again being revealed.

It is irresponsible to continue to fuel the boom in Germany - by far the largest economy in Europe - with zero interest rates because the economy in the southern states is growing only weakly. Did monetary policymakers learn nothing from the years before 2007, when Germany, the sick man of Europe, needed low interest rates and these then triggered a credit-financed construction boom in Ireland and the southern states? What is particularly absurd is that many German politicians now also want to step on the gas in terms of fiscal policy - after all, choice is what presents are needed for. How all this will end in 2018 or 2019 can be looked up in any economics textbook. Keyword: economic cycle.

What does this mean for the stock market? Nothing has changed in our basic scenario. The German equity market continues to benefit from the historically unique combination of boom and zero interest rate. However, the situation is worsening. After all, the future is being paid for on the stock markets. And the rule is: If things can't get much better, they'll probably get worse.

The nervous reaction to Mario Draghis' positive comments on the economic situation in Europe shows that market participants are well aware of this. It was increasingly based on a broad foundation. A signal for a turnaround in interest rates? "We need perseverance in monetary policy," reassures Draghi. The head of the central bank did not want to talk about a tightening of monetary policy - i.e. the "increase" of the deposit rate from a completely absurd minus of 0.4 percent to absurd zero percent.

It is almost tragic that the ECB President is discovering positive developments in the economy at the very moment when the German economy is apparently gradually approaching a cyclical turnaround.

This does not have to happen immediately. An economic turnaround is only to be expected once ifo business expectations have declined three times in a row. The ifo indicator can fluctuate back and forth in the boom territory for some time until such a signal is received. The indicator showed similar values to those of today, for example, most recently at the turn of the year 2006 to 2007. At that time, the economy did not turn around until half a year later. And the DAX - starting from an already very strong overvaluation - had climbed by a further 15 percent by then.

In this context, however, an analysis by HELABA is also interesting. It examined how the DAX developed after the ifo index had reached spheres as airy as today. The result: On average, the DAX yielded a return of 4.1 percent in the following twelve months. If things don't get any better, they just get worse.

The private-wealth stock market indicator takes obvious risks into account. In view of the very ambitious valuation of many German shares, the model continues to propose "only" a 60 percent equity quota of the equity portion that the respective investor considers to be appropriate in the long term. An investment in stocks today is clearly a dance on the volcano. But this one doesn't have to be over yet.

yours

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided in private wealth is for information purposes only and does not constitute an invitation to buy or sell securities.