Structural Reform.

Secondary Private Equity. In times of low interest rates and high valuations on the stock markets, classic portfolios of shares and bonds no longer work as well as they did in the past. "I therefore advise restructuring the portfolio," explains Florian Dillinger, Matador Partners Group: "Private equity, the participation in unlisted companies, stabilizes and increases the return."

"Take a little trip back in time with me to the year 2031," prompts Florian Dillinger, Matador Partners Group, "and consider what returns will probably be achieved in the individual asset classes in the coming years."

In the bond sector, the pro says, that's pretty straightforward. "Even if we come out of the negative interest rate era very slowly, it's not likely to be more than one to two percent with high quality bonds - at best." And even in the stock market, the trees are unlikely to grow to the sky as they have in the past. "At some point, the current high valuations will normalize. That's why many professionals assume that equities, too, will only yield five to six percent per annum on average instead of the usual eight to nine percent."

For investors who have long made around seven percent returns with a traditional 60/40 split between stocks and bonds, this is creating an "aha" effect. "Over the next ten years, it's probably only going to be four percent," Dillinger calculates, concluding, "Investors either have to lower their expectations or change their portfolio structure - and in the best case, do it in a way that increases returns without increasing volatility."

Sounds a bit like squaring the circle. "But it can be done by reallocating a 20 per cent share - ten per cent equities and ten per cent bonds - to private equity. This new structure makes a portfolio sustainable. Because private equity should bring more returns than equities - and with less fluctuation."

Detlef Mackewicz, Managing Director of Mackewicz & Partner and consultant at Matador, explains that two factors are primarily responsible for this: "A broader investment spectrum and active management of the property."

In the U.S., for example, 95 percent of companies are privately held, according to UBS. Through the vehicle of private equity, investors can participate in exciting business models to which they would otherwise never have access. By taking a significant stake, managers of private equity funds are also able to initiate changes in strategy or operations, directly contributing to value creation. "This is a key difference compared to equity investing," clarifies Mackewicz.

Indeed, private equity returns then also averaged between 7.6 and 14.5 percent. "And the fact that investors' nerves were spared in the process is quite simply due to the valuation method," adds Mackewicz. "Whereas market prices for stocks and bonds are determined every second and massive over- and undervaluations therefore occur, the value of private equity investments is only determined on a quarterly basis. That's why investors don't feel the fluctuations. Psychology, which is often such a drag on the stock market, doesn't play a role here." "And because of the illiquidity, they are not even tempted to sell at the wrong time for mostly unfounded, purely stock market psychological reasons," adds Florian Dillinger.

In view of these advantages, it is not surprising that private equity has become a great success story. Never before has so much money flowed into this sector. "Unless some other catastrophe occurs in the few weeks of the current year, 2021 will set a new fundraising record," informs Mackewicz.

While the fact that a lot of money is currently being raised is good for the sector, it also poses risks for investors. "There is already a risk that managers will overlook many a weakness in companies when buying. The combination of a lot of capital and low interest rates, coupled with some investment pressure, can lead to increased risk appetite," Dillinger reflects.

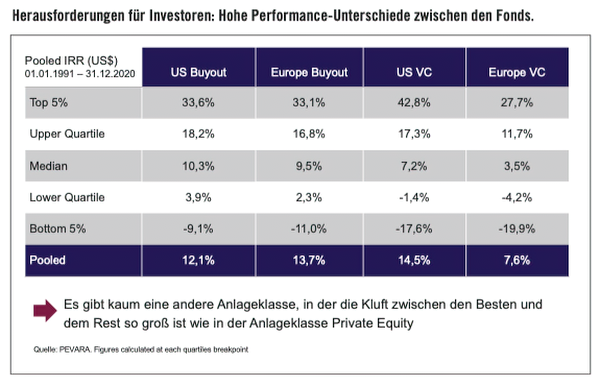

From an investor's perspective, therefore, even more caution than before is called for. "In no other asset class are the differences between the results of the best and the worst funds as large as in private equity. While the top five percent of funds achieve annual returns of well over 20 percent, the returns of the worst five percent, however, also reach into negative territory," analyzes Mackewicz.

For investors in private equity funds, it is therefore a major challenge to select those that can form a stable and balanced portfolio from the annual offering of around 1,000 funds currently being fundraised. "Even professionals often spend weeks on fund selection and have to ask themselves numerous questions at different levels," explains Dillinger (see chart below).

But there are even more hurdles: Investors with a track record of successful private equity programs have broadly diversified their investments and, most importantly, spread them across all vintages-regardless of the current economic climate. Such a portfolio, covering venture, small, mid, large and mega buyout segments as well as the US, Europe and Asia regions, can easily include 20 to 30 fund investments. "The amount of work for the investor is then enormous. And building such a portfolio requires a significant amount of capital," explains Dillinger.

Even those who manage to do this haven't won. "The most successful private equity funds only take on a few large investors. They are generally not interested in many small ones," Dillinger explains.

For private investors to get involved there, so-called feeder funds have to be created first. These are offered by banks, asset managers and issuing houses.

For the initiators concerned, this is an attractive business model. "For the investor, however, this does not apply without restrictions," clarifies Dillinger, "because the additional structures are often associated with high costs. And these - issue surcharge, annual management fee, profit sharing - naturally reduce the private investor's return." "Let's assume that a professional institutional investor achieves an average of ten to twelve percent net return per annum across all market phases with a well-balanced private equity program," Mackewicz reflects, "Even if the private investor had the same private equity funds in his portfolio, his return would probably be four to five percent lower because of the costs for the intermediaries. The net return would probably only be between five and eight percent."

"At that point, structural reform would be of little use. That's why Matador Partners Group gives its shareholders access to a private equity portfolio with an excellent track record and attractive dividend yield at a low cost," explains Dillinger, concluding, "A portfolio of 50 percent equities, 30 percent bonds and 20 percent private equity should thus again create around six percent returns over the next decade."

-----------------------

Secondaries - investing intelligently in private equity.

The listed investment company Matador Partners invests primarily in so-called secondary private equity funds. Compared to primary funds, this offers five interesting advantages:

Firstly, capital is drawn down more quickly in the case of secondary investments. This results in an accelerated build-up of assets. The J-curve effect common with primaries is mitigated or completely avoided. Not only can investors expect earlier returns, they also have a broad portfolio of funds of different vintages, regions and styles at their immediate disposal.

Second, secondary fund managers are not buying a black box. The assets are already in the fund and can be well valued. This reduces risk and is particularly important in venture capital because for many startups, it becomes obvious in the first few years whether they have a real opportunity.

Third, it allows the investor to blend in vintages of funds that are no longer available on the primary market.

Fourth, the costs are lower because the fund has a shorter remaining life and the management fees of the first years have already been paid by the original investor who is now selling his shares.

And fifth, the transaction often results in discounts to the presumed value of the company because a seller wants to part with his stake and is therefore willing to make concessions on the price.

In the past, this strategy has worked extremely well. "We have been able to achieve a net average return of 12.8 percent per annum over the past 15 years," informs Florian Dillinger. Matador is currently involved in 23 private equity funds with a total of around 1400 companies.

The shares of Matador Partners Group are traded on the home exchange BX Swiss (ISIN: CH0042797206). Through this vehicle, a broadly diversified secondary portfolio without minimum investment restrictions is available to all interested investors. In the last two years, the share price has risen from 3.50 to 4.44 Swiss francs.

-----------------------

®

Special Publication:

Matador Partners Group AG

Grundacher 5, CH-6060 Sarnen

41 41 662 10 62