Now more than ever.

Hotel real estate. The hotel and travel industries are at the epicentre of the Corona crisis. "Although the short-term outlook is extremely bleak. But those who invest countercyclically in hotels will be rewarded in the long term", Philipp Ellebracht, Head of Real Estate Product Continental Europe at the Schroders investment house, is convinced: "Because the hotel market should have fully recovered within the next five years".

Hotel real estate. The hotel and travel industries are at the epicentre of the Corona crisis. "Although the short-term outlook is extremely bleak. But those who invest countercyclically in hotels will be rewarded in the long term", Philipp Ellebracht, Head of Real Estate Product Continental Europe at the Schroders investment house, is convinced: "Because the hotel market should have fully recovered within the next five years".

The legendary US investor Warren Buffett once said that there are times when fear paralyzes investors. Then you have to buy. His message: "Be greedy when others are afraid, and scared when they are greedy."

The hotel sector is clearly one of the economic sectors in which fear and uncertainty are extremely pronounced today.

Many hotels, especially those geared to international tourism with a thin equity base, will face serious financial problems and significant restructuring. As a result, a market shakeout is expected in a few months. "Then we will be ready with interesting investment strategies to take advantage of opportunities," analyses Philipp Ellebracht, real estate expert at the Schroders investment house.

Schroder Real Estate has been investing in hotels across Europe for more than 18 years. Has managed the SARS epidemic, the terrorist attacks in Paris, Brussels, Barcelona and London. And is convinced that people will travel again even after the global pandemic. "The longing for distant lands is deeply rooted in us. Daher I think that the long-term upward trend in tourism will only get a kink - albeit a deep and broad one. But after that it will continue with private and business travel. Certainly, some business meetings will become obsolete and will be carried out via digital telecommunication channels, but the global growth, especially in the Asia-Pacific region, will more than compensate for this. Anyone who thinks long-term should therefore make bold use of emerging opportunities in the hotel segment".

These opportunities, Ellebracht is convinced, will open up in the coming months. In the past, many hotel chains and financial investors have increased their debts in view of ultra-low interest rates. Now income is falling in the short and possibly even in the medium term, interest and repayments can no longer be serviced. Those who had only a medium to good occupancy rate in the run-up to the crisis will now have to give up.

"In the future, the prices for hotel properties could therefore fall temporarily", Ellebracht is convinced, "and this will hardly be absorbed by the enormous sums of money from opportunistic private equity companies. Only those investors will profit who, like us, are in a position to constantly adapt hotel operations to the new challenges.

However, it is not only a favourable purchase price that makes this real estate segment particularly interesting for professionals at present. "It is at least as important that we are now getting hotels in locations where there used to be no offer at all. In many European cities we will also notice an undersupply of hotel capacities in the long term - examples are Paris and Amsterdam. The restrictive local regulations often do not allow new buildings in the historic city centres. However, tourists and also business people want to stay in the city centre and are reluctant to stay in peripheral locations. Due to the upheavals caused by the COVID 19 crisis, we will be able to identify investment opportunities that simply did not exist before".

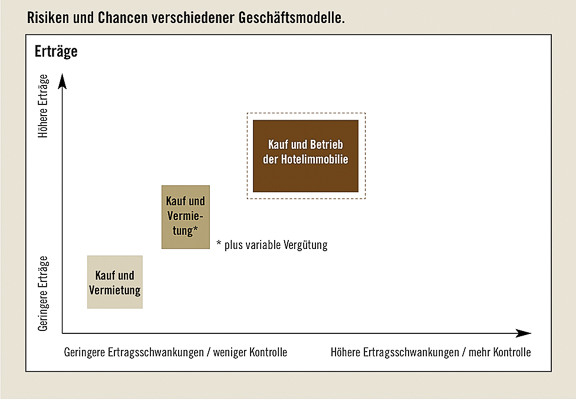

Investment opportunities in hotel real estate usually take place between two large segments, which differ significantly in terms of opportunity and risk.

The first, less complicated option is to buy a hotel with an existing lease. Die Lease is then paid by the hotel operator. "The selection criteria are apparently obvious here", explains Ellebracht: "Among other things, the location of the hotel, the operator's creditworthiness or the building and its long-term use are important."

However, the fact that the creditworthiness of the operator chain - Hilton, Marriott or Arcor - can be easily checked also involves risks. "The ratings suggest a supposed security. But we know from experience that this can be deceptive. The hotel's own creditworthiness checks and verification of its profitability remain irreplaceable even with this variant", macht Ellebracht clearly states.

The other pole of the investment universe lies in the area of management contracts. Here the investor acquires not only the property but also the entire hotel operation, including responsibility for the employees. The crucial thing now is to understand the operational relationships: How do I gain market share? What should overnight stays, spa, bar or restaurant revenues bring in a particular location? And what must an investor do to achieve such goals? "It may be necessary to completely rebuild the hotel, to establish a new gastronomic concept or a different operator brand. Anyone who buys a hotel in a good location and does not shy away from the risks of running a hotel will make disproportionately high profits as the recovery phase progresses," explains Ellebracht.

Because this is much more difficult than "buy and let", only a few investment teams in Germany are able to do so. "We have been able to do this throughout Europe for over 20 years!"

Between these two poles, there are also hybrid investment models in which the owner also leases to an operator. However, only 80 to 90 percent of income is generated from rental income. Ten to 20 percent - the icing on the cake - comes from management income. If the hotel's income fluctuates, of course, this also varies.

"In order to be able to estimate at the time of purchase how sustainable this 20 percent is and how this percentage can be improved, it is also important to know exactly how to operate a hotel," explains Ellebracht and talks about an engagement in Nice. There, he says, the management earnings were low because the food and drink division was obviously poorly managed. The Schroder experts found that the pool on the roof was hardly used. They invested 150,000 euros - which is not much for a hotel - and refurbished the pool and rooftop bar.

"Today, this is a real hot spot. And the hotel makes 1.5 million euros more turnover per year with a 20 percent increase in yield. If you know the right parameters, you can achieve a lot with small changes.

Even in the apparently simple letting business, know-how often makes the difference. Schroders, for example, is one of the major landlords of the Marriott hotel chain in Europe, which means that it knows the concepts of operators and can better assess the risks of rental agreements. "As owners, we receive the sales figures of the individual hotels every week. If we notice anything, we call and make suggestions for improvement. And if the operator - in extreme cases - slides into insolvency, we could even run the hotel ourselves for a transitional period. This is an additional, important safety net for our investors.

Using this knowledge in the operation of a hotel as an investment manager and creating value from it is what fascinates Ellebracht most. "The hotel team had, for example, bought the Westin in Venice, directly on the canal, some time ago," the professional explains. Because the location is unique, Schroders wanted to change the operator and turn the hotel into a luxury hotel. The entire hotel was renovated, repositioned and raised from four to five-star standard. "This was a core refurbishment. New architecture, design work, lighting concepts. Eine Bar, designed by the hottest architects in London. It's pretty cool what our project teams can come up with."

The question of the future hotel brand was at the centre of attention. The hotel experts had the St. Regis hotel chain in mind, one of the most luxurious hotel brands in the world. Through the acquisition of Starwood, it belongs to the Marriot Group. "In October 2019, the St. Regis opened in Venice. The fact that we were able to pull this off is demonstrated by the outstanding quality of our hotel team, led by Frédéric de Brem, our Head of Real Estate Hotels."

In a few years, the real estate professional is convinced that he will have many similarly exciting stories to tell. Most likely, there will also be some anecdotes about the investments of the upcoming Corona clean-up. Because after the pandemic, Ellebracht is convinced that the tourism industry will return to its old growth path. The most important driver will continue to be the growing prosperity of the population in Asia. When asked what they would do with additional money available, China's consumers answered in a survey by HSBC with an overwhelming majority: "Travel.

"And the preferred destination is Europe. It is obvious that especially European hotels with a strong equity ratio will profit from the distortions. They will gain market share in the consolidation process, increase occupancy rates and revenues per room", Ellebracht is convinced and concludes: "Of course this will take time. Slowly, step by step the hotels will reopen. This process also varies from country to country. And it will take time for tourists to dare to travel again and for flight connections to be available in the usual variety. But we will use this time - to research, select and invest in the most promising hotels".

_____________________________________________________

How to invest - in hotels.

The investment and asset manager Schroder Real Estate focuses on two European investment strategies for hotel properties:

As part of its active strategy focused on management and operational risks, Schroders buys and operates hotel properties. The fund has already raised €350 million in equity capital and will be closed when the €500 million threshold is reached. The capital will be invested in ten to 15 hotels over the next 24 to 36 months. The term of the fund is to be eight to ten years. During this time the hotels are to be optimised and then sold at a higher price. "The fund is therefore more comparable to a private equity engagement", explains Ellebracht.

The hotel is currently working on a second strategy. This involves the acquisition of hotel real estate, which is primarily focused on income from leases. To a small extent, management income will also contribute. "It will be a so-called evergreen strategy - that is, an investment with no time limit. The purchase volume is between 40 and 80 million euros per hotel. We are aiming for annual distributions of between four and five percent."

In both strategies Schroder Real Estate concentrates on the leading European destinations. It is important that the respective city is a destination for both business and tourism clients, so that the investment can benefit from two different income streams. "Furthermore, we only invest in hotels with three to five stars. This segment accounts for around 70 percent of total hotel sales. Unserer Experience shows that the substance of the land and building values in this segment is better and the revenues are much more resistant to market fluctuations", erklärt Ellebracht.

Sustainability also plays an important role. As a pure owner, Schroders relies on LED lamps, good heating, natural air circulation or window insulation to save energy.

Where the hotels are managed by the company itself, the possibilities of influence go much further. This is also where an attempt is made to involve hotel guests in the topic by means of education. "Our declared aim is zum Beispiel to push down the current standard of 'one kilo of laundry per day and guest per star'," Ellebracht explains.

_____________________________________________________

Hotel investments à la carte.

Anyone interested in investing in hotels can choose from a wide range of different risk/reward profiles.

The easiest way to buy a hotel property is to buy it and then lease it to an operator. According to Schroders, returns on capital employed (IRR) of between five and six percent have been achieved in the past. Due to the current crisis situation, perhaps one to 1.5 percentage points more can be achieved next year. "In the medium term, however, returns will then decline again," Philipp Ellebracht suspects.

Such an investment is interesting for cash flow-oriented, professional investors, pension funds or insurance companies with regulatory requirements regarding their suitability for real estate quotas.

The greatest opportunities, but also the highest risks, are offered by investments in vehicles that buy and operate hotels. Here, according to Schroders, the return on capital employed has been much higher in the past and predominantly in the double-digit range, but with significantly higher risk. And here, too, a significant increase is possible due to the market distortions. The most important criterion for this investment, which is particularly interesting for private individuals willing to take risks and family offices without regulatory requirements, remains the know-how of the investment house.

Between these two poles, there are hybrid models. Here the investor is the owner of the property and part owner of the operational business.

_____________________________________________________

®

Special publication:

Schroder Real Estate Investment

Management GmbH; Taunustor 1;

60310 Frankfurt am Main

www.schroders.com/de/de/realestate/

Philipp Ellebracht

49 (0) 69 975 71 78 16