A race against time.

After the business cycle component of the private-wealth stock market indicator delivered a buy signal last week, we received many enquiries from the network. How can it be that the outlook in industry is improving while new orders - an important leading indicator - are declining significantly?

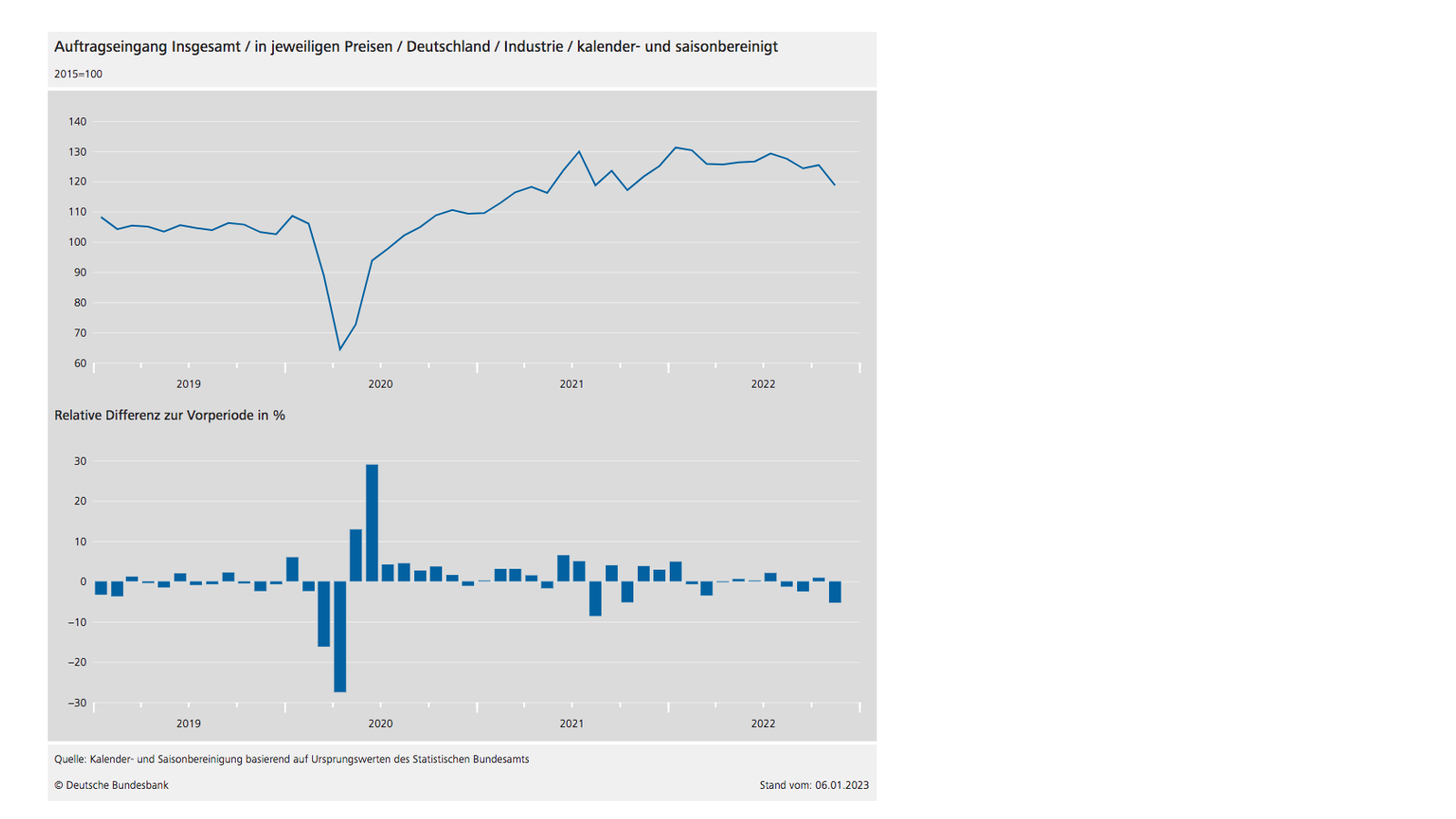

Indeed, new orders do not look good. Since the beginning of '22 they have been showing a clear downward trend, both from abroad and domestically. Especially in real terms - i.e. in terms of pure volume - there is a clear slump (see chart below). And because volume is a decisive factor for capacity utilisation and thus to a large extent also for profit margins - this is a development that can cause concern for investors.

It is interesting that the orders at the respective prices are still reasonably stable (chart below). So the companies are apparently succeeding so far in pushing through price increases.

The fact that the poor order trend has not yet had a negative impact on production across the board is due to the very comfortable order situation in the industry (chart below).

The volume of orders had increased dramatically in 2021 and is still around 25 percent above the "normal level". For a long time, this order mountain could not be cleared due to material bottlenecks and delivery difficulties.

This is now changing. Since September last year, the order backlog has been worked off, thus compensating for the weak incoming orders.

This effect should continue for a while. But of course it won't work forever. By spring/early summer at the latest, new orders would have to pick up again if a deeper recession and a corresponding slump in profits at companies in Germany are really to be avoided.

Accordingly, we are looking forward to the next figures on incoming orders. Unfortunately, these are always announced with some delay. For example, the December data will be published on 6 February. The development in January and February will be reported on 7 March and 5 April. Then at least a stabilisation in the volume of orders should become visible. The 2023 business cycle will definitely be a race against time as well.

Yours sincerely,

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided in private wealth is for informational purposes and is not an invitation to buy or sell securities.