Between hope and sorrow.

Dear Readers,

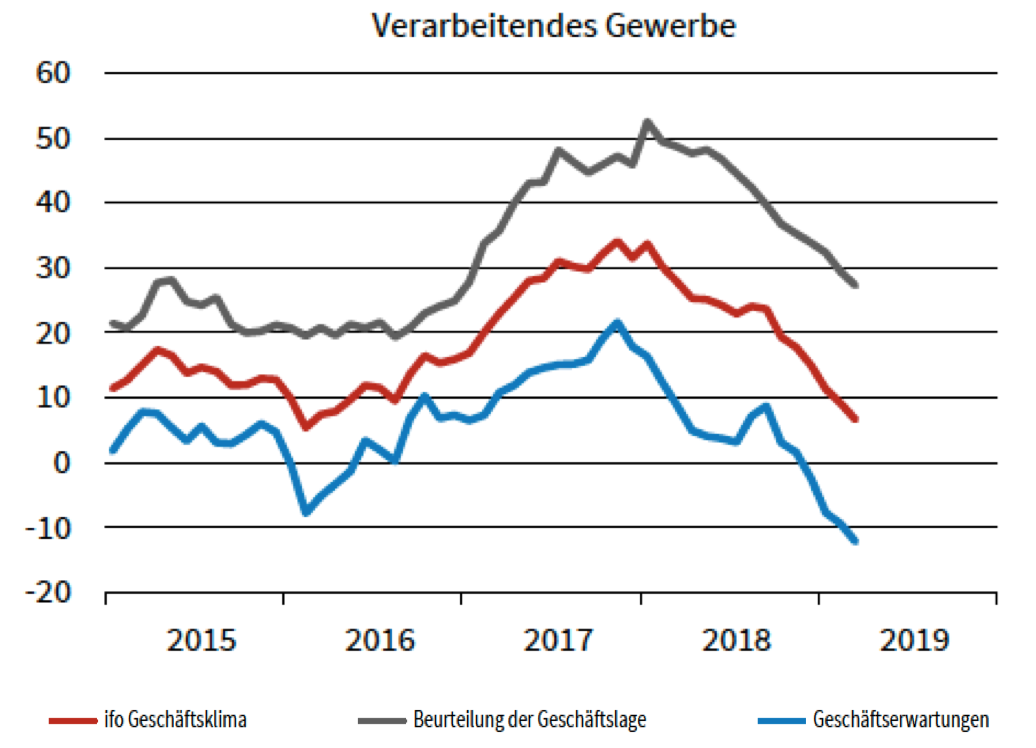

The ifo business climate rose in March for the first time in six months. This, at first glance, good news, however, is put into perspective when looking at the individual areas. The service sector, trade and construction were responsible for the increase. In industry, which is regarded as a sentiment indicator for the global economy and the stock markets, the decline continued steeply (Chart 1). The expectations of entrepreneurs in the manufacturing sector have now reached their lowest level since November 2012.

The ifo business climate rose in March for the first time in six months. This, at first glance, good news, however, is put into perspective when looking at the individual areas. The service sector, trade and construction were responsible for the increase. In industry, which is regarded as a sentiment indicator for the global economy and the stock markets, the decline continued steeply (Chart 1). The expectations of entrepreneurs in the manufacturing sector have now reached their lowest level since November 2012.

Pessimism in industry is also reflected in export expectations. They virtually collapsed in March (chart 2).

A glimmer of hope comes from China. We pointed out last month that most economists expect the global economy to recover in the coming months because China is stepping on the gas again via both monetary and fiscal policy. At least the early indicators there are now showing an initial improvement. If it is true that a large part of the weakness in the industry was due to the problems in China, then expectations in the industry should soon also brighten up.

Share prices are therefore already rising on the capital markets. Investors are looking through the current economic weakness and are positioning themselves for stronger growth in the second half of the year. News that the trade dispute between China and the U.S. may be over soon will further boost optimism. Dent instead of recession is the unanimous verdict.

That's a tricky starting position. If the dell theory is indeed confirmed in the coming months, the private-wealth stock market indicator would probably react too slowly and miss some of the price gains. The indicator is a very long-term model, which above all keeps an eye on the risks. Clear improvements must first be seen before the indicator abandons its defensive stance.

This cautious attitude is currently also supported by capital market seismographs. As you know, it distinguishes between three phases: "green" (quiet market = buy), "yellow" (turbulent market with positive expectation = invest, but with hedge) and "red" (turbulent market with negative expectation = do not invest).

In the last weeks the probability for a bear market (red) had successively decreased. In recent days, however, this positive trend has reversed. In the meantime it has risen again to 40 percent. The probability of a calm, positive stock market ("green, buy or hold") is 48 percent. The probability of a turbulent, volatile market with positive trend ("yellow") at 12 percent. The underlying sentiment, which was very positive in the recent past, has returned to normal," explains Oliver Schlick, who concludes: "If the currently still weak fundamental data does not improve, there is a risk that the probabilities derived from it could further deteriorate. Overall, a somewhat less offensive portfolio allocation can be derived.

Conclusion:

The private-wealth stock market indicator has been out of the stock market since the end of February 2018. This was triggered by the three-fold decline in ifo business expectations in the industry and the simultaneous very high valuation of the stock markets. Since then, the indicator has proposed a minimum weighting of equities of 0 - 30 percent of the individually planned equity component.

For the short-term positioning within this corridor we use the results of the capital market seismograph. As this has now deteriorated again somewhat, the proposed equity ratio will fall from 30 to 25 percent.

yours

Klaus Meitinger

Note: Despite careful selection of sources, no liability can be accepted for the accuracy of the content. The information provided in private wealth is for information purposes only and does not constitute an invitation to buy or sell securities.